Bloomberg New Energy Finance reports that Danish wind manufacturer Vestas reclaimed the top spot in the annual ranking of wind turbine manufacturers.

Top Onshore Turbine Manufacturers, 2016

BNEF 2017

🇩🇰 Vestas has been on the scene since 1945 as an appliance manufacturer and moved into turbine production in 1979 and has plants in Denmark, Germany, India, Italy, Romania, the United Kingdom, Spain, Sweden, Norway, Australia, China, and the United States. They installed a whopping 8.7GW of turbines in 2016, good for 16% of all onshore wind installations last year. 43% of those 8.7GW were in the USA. Vestas has a very international reach and is continuing to pursue a global strategy with projects commissioned in 35 countries, more than any other turbine maker.

🇺🇸 General Electric placed second with 6.5GW, some 0.6GW more than in 2015. They are the largest producer in the USA and while they narrowly lost its traditional lead in the US market for newly commissioned turbines to Vestas, GE managed to increase its global presence to 21 countries in 2016, from 14 in 2015.

🇨🇳 Xinjiang Goldwind Science & Technology fell from first to third place with 6.4GW in 2016. Virtually all of the Chinese manufacturer’s capacity was built in its home market, where Goldwind further extended its market share. China’s contracting wind market had a clear impact on Goldwind, as overall installations were 22.8GW, down 21% from the record 29GW in 2015.

🇪🇸 Gamesa came in fourth and reported that it had beaten its own annual turbine manufacturing record, having already made more than 1,880 units with a total productive capacity of 3,880 MW. The new record was a long time in the making, taking eight years to beat 2008’s 3,787 MW. Their record was set with turbines assembled all over the world — India (36%), Europe (28%), China (26%) and Brazil (10%). Almost one in three Gamesa turbines was installed in India.

🇩🇪 Enercon sits in 5th place, with a market share of 7.2% worldwide and 59.2% only in Germany. Enercon has production facilities in Germany, Sweden, Brazil, India, Canada, Turkey, and Portugal. They are limited to onshore wind turbines.

🇩🇪 Nordex, in 6th place has installed wind power capacity of more than 18 GW in over 25 markets. The production network comprises plants in Germany, Spain, Brazil, the United States and soon also India. Nordex closed the first half of 2016 with a new record in German installations, with a total 134 new turbines installed marks an increase of 135% over the same period in the previous year

🇨🇳 Guodian / United Power is the Chinese runner-up, with its manufacturing spread entirely across China. Originally, a joint venture with Westinghouse and later a joint venture with Siemens from 1998 to 2006 before restructuring to a state-owned enterprise in 2007. Today, they have 23,030 MW of wind power installed, they have grown rapidly and strategically in the last 15 years.

🇩🇪 Siemens Wind Power in 8th place seems to be coming in short, but this is because this list looks at onshore wind, whilst Siemens supplies about 60% of European offshore wind turbines.

🇨🇳 Ming Yang 明阳风电 is the largest privately owned wind turbine manufacturer in China.

🇨🇳 Envision, the “smallest” Chinese entrant, Since its foundation in 2007, Envision Energy has maintained rapid growth in its business operations.

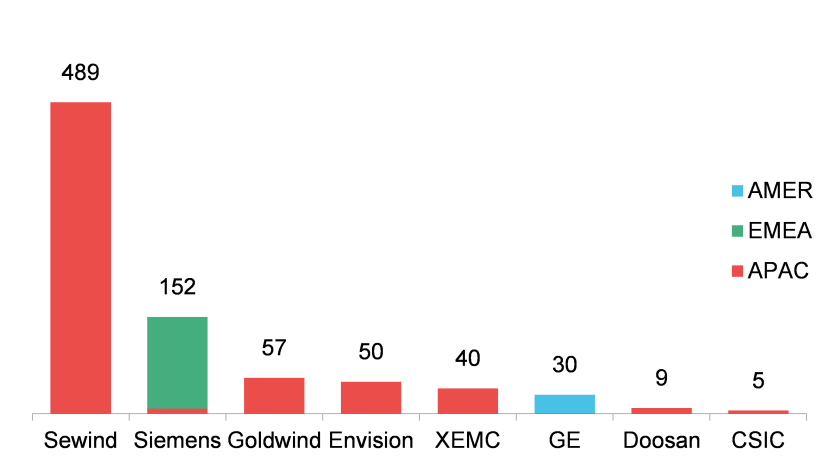

Top Offshore Turbine Manufacturers, 2016

BNEF, 2017

🇨🇳 Sewind is the undisputed offshore leader, supplying nearly 60% of the 832 MW of new offshore wind turbines commissioned in 2016 globally and since it manufactures Siemens offshore turbines under license in China, the company actually installed 388 MW of Siemens turbines and 101 MW of own design machines.

What to expect next

I wrote about the upcoming merger between Gamsea and Siemens a few months ago here and the merger between the two is set to go through. It appears that they are aiming at speeding up consolidation due to competition and price pressures. As Gamsea and Siemens combine their wind-turbine manufacturing businesses, creating a company that will dominate the industry, Vestas will be dethroned to second place.

A recent report by the Global Wind Energy Council (GWEC) shows that China installed 592 MW of offshore wind in 2016, entering the global top three alongside Germany and the Netherlands. Although the GWEC and BNEF reports focus on different aspects, both point to a steady rise in Asian offshore wind markets. This is also evident in day to day new reports on deals and contracts.

There are some interesting developments in terms of who’s got skin in the equity game in renewable energy. What’s really interesting to me is that the equity investment landscape has transformed quite a bit in the last few years and in this post we’ll see how and why.

But first, remember that, according to the OECD, there are three (main) ways to finance renewable energy projects:

Project Finance: This involves a mixture of debt (usually from banks) and equity capital (we will go into more detail below). According to Bloomberg, 2015 was the first year in which project finance constitutes more than half of total asset finance in RE electricity. Remember that project finance involves creating a Special Purpose Vehicle (SPV) with its cash flows separated from those of its sponsor companies;

On-the-balance sheet financing: Done by utilities (EDF, ENEL, Suez), independent power producers and other project developers. On the balance sheet financing, makes up over 47% of total asset finance in RE, about 94 billion;

Project Bonds: Project Bonds, these do not include corporate bonds or government bonds. They account for a small fraction of financing.

Nevertheless, there are other emerging financial structures, which I can go into in another post, but venture capital is one of them. Utilities are substantial providers of equity capital in the renewable sector. However, due to the large scale investment and stable income returns, there is greater interest from the financial services industry.

This brings us to wind equity financing

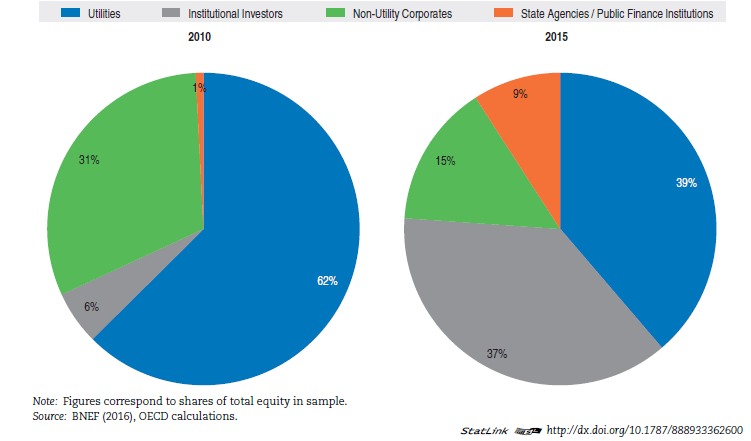

Back in the day, the first offshore wind-power farms were usually financed on the balance sheets of the utilities that planned, built, and operated them. Today, there are many more players involved, such as banks, private equity funds, pension funds, state-backed “green” banks (such as the Green Investment Bank, the Nordic Investment bank and the European Investment Bank) and insurance companies. The graph below shows how the equity mix has morphed in the last couple of years.

Change in Equity Mix for Wind Energy

The share of equity provided by utilities is steadily shrinking as other players get involved, decreasing from 62% in 2010 to 39% in 2015, and that of non-utility corporates from 31% to 15%. In other words, the combined share of the two traditional equity investors in the wind energy sector decreased substantially, from 93% in 2010 to 54% in 2015. Accordingly, other investors have stepped up their game. One of the possible explanations for this decrease may potentially be due to deleveraging as a consequence of the financial crisis.

The Rise of Institutional Investors

For brownfield wind projects, meaning wind projects where there is already existing infrastructure and possibly licenses as well, institutional investors such as pension funds, insurance companies, private equity and infrastructure funds have become major equity investors. According to the OECD, their cut in total equity provisions increased from 6% in 2010 to a staggering 37% in 2015, making them the second most important equity providers in the 2015 sample, just 1% behind utilities. This sharp increase of equity provision by institutional investors can be traced mainly to the acquisition of brownfield assets or portfolios for onshore wind deals. Pension funds and insurers were not involved in any greenfield onshore wind-power transactions included in the OECD 2015 sample.

This trend suggests that institutional investors look to the onshore wind sector mainly for the acquisition of existing projects.Such a strategy presents several advantages:

Lower Costs: Existing projects are already (usually) built, and there they do not need to start from scratch;

“Up to Code”: Lengthy permits, licensing and commissioning agreements may already be in place and therefore do not need to be requested;

Fast Deployment: Ultimately the project can be up and running (and earning) in less time.

Moreover, equity financing in wind energy assets by state agencies and public finance institutions grew from a negligible cut in 2010 to 9% of total equity invested in 2015. This sharp increase can be linked directly to the investments done by the UK Green Investment Bank. The UK’s GIB, an institution created by the UK government in 2012 with the aim of attracting private sector financing for green infrastructure projects. The creation or expansion of similar institutions is a trend observable at the global level and is important for risk sharing with newer technologies. Take offshore wind, for example, as projects scale up and move into deeper water, newer technologies also add to construction risk. This may be a barrier to entry and discourage some investors from participating.

In Europe, commercial banks have started partnering up with government supported banks (United Kingdom’s Green Investment Bank, Germany’s KfW Development Bank), export credit agencies (Denmark’s EKF and Belgium’s Delcredere – Ducroire and Italy’s SACE), and multilateral banks (the European Investment Bank) as a way to provide equity financing to wind projects .

The diversification of participants is good for everyone, because:

Risk: The risk that corresponds to the project is diversified across an array of investors, meaning that investors are more likely to invest if they do it along other reputable investors, rather than going in it solo;

Mainstreaming: the diversification of participants shows that equity financing for RE is no longer as niche as it was, with pension funds and insurance companies putting skin in the game.

Example: The Galloper Offshore Wind Farm

The largest wind equity deal in Europe in 2015 the the Galloper Offshore Wind Farm. It’s a project that will be completed in 2018, located off the coast if Suffolk, east England.

The equity investors are:

Innogy RenewablesUK, a subsidiary of the German utility company RWE

The UK’s Green Investment Bank, a public finance institution

Macquarie Capital, an institutional investor

Siemens Financial Services, a subsidiary of Siemens, a corporation

Sumitomo Corporation, a corporation

This array of private and public investors is an example of what the equity landscape is shifting towards.

So why did the equity investing landscape change?

The explosion of new capacity additions fostered equity market growth for wind projects. New projects not only became more frequent but they also grew in average size, requiring more capital. It would only be normal to have several new, independent developers enter the sector under such favorable market conditions. Moreover, many utilities have been financially constrained due to the difficulties in the merchant power sector, further limiting their contribution to the sector.

The take-home message we can draw from this is that as the demand for wind energy increased so did the associated capital requirements. Utilities and developers did not have the necessary capital to cover demand, so third party investors were roped in. Likewise, corporations like Siemens and Sumitomo are using their financial strength to offer financing directly to smaller developers.

Preamble: I would like to point out that I truly prefer not to engage in these types of discussions (read: I’m over it), because the sources of information that are available to me, are available to everyone else. I also do not consider it my duty to educate every Tom, Dick, and Henry on climate change. However, in light of recent developments, we will probably be encountering a more energized brand of deniers, so here is a non-exhaustive list of answers I took from Robert Henson’s Rough Guide to Climate Change.

Since the days of Roger Revelle, the pioneering oceanographer whose body of work was instrumental for our understanding of the role of greenhouse gas emissions in our atmosphere, deniers developed certain criticisms that are still popular today. I believe that these arguments will keep on cropping up for as long as there is a “debate” on climate change, so it’s best that we equip ourselves with appropriate answers.

Taken to the extreme, anti climate change arguments can be summed up in the following quote:

“The atmosphere isn’t warming; and if it is, then it’s due to natural variation; and even if it’s not due to natural variation, then the amount of warming is insignificant; and if it becomes significant, then the benefits will outweigh the problems; and even if they don’t, technology will come to the rescue;and even if it doesn’t, we shouldn’t wreck the economy to fix the problem when many parts of the science are uncertain.”

Toles 2006, Washington Post

“But the atmosphere isn’t warming….”

According to an ongoing temperature analysis conducted by scientists at NASA’s Goddard Institute for Space Studies (GISS), the average global temperature on Earth has increased by a mean of about 0.8° Celsius (1.4° Fahrenheit) since 1880. Two-thirds of the warming has occurred since 1975, at a rate of roughly 0.15-0.20°C per decade.

This arguement, has seeminly been put to rest, yet deniers seem to resist it, possibly because they do no think that a global mean warming of 0.8°C is a big deal. Here is a more vivd statistical example of what that means:

Dr. Arun Majumdar’s presentation, Michigan State University

This is a bell curve mapping distribution of temperature anomalies over 60 years. To the left are temperatures colder than average and to the right are temperatures hotter than average. The mean is shifting and the distribution is broadening rightwards. The right tail of the distribution is reaching 4 and 5 sigma, which are probabilities that were unheard of decades ago. The anomalies occurring at 4 and 5 sigma are (were) rare massive heatwaves, storms, and floods, which are becoming more common then ever.

“Okay, but I still went skiing this winter…”

The weather and the climate are two different things. The difference between weather and climate is a measure of time. Weather is what conditions of the atmosphere are over a short period of time, and climate is how the atmosphere “behaves” over relatively long periods of time. We talk about climate change in terms of years, decades, and centuries. The weather is forecast 5 0r 10 days ahead, but the climate is studied across long periods of time to look for trends or cycles of variability, such as the changes in wind patterns, ocean surface temperatures, and precipitation. Snow in skiing locations isn’t proof that climate change is not happening.

“The warming is due to natural variation…”

This is a very common argument, the denier does not argue against the existence of climate change, generously admitting the climate has *always* changed, but they do not believe that humans are responsible for it.

The IPCC has concluded that the warming of the last century, especially from the 1970s, falls outside the bounds of natural variability.

Variation of Co2 in atmosphere, from 800000BC to today, NOAA NCDC

Let’s walk down memory lane and look at what the IPCC has been saying to us for 26 years. And keep in mind that the IPCC reports are the most comprehensive, global, and peer-reviewed studies on climate change ever written by anyone, bringing together the work of over 800 scientists, more than 450 lead authors from more than 130 countries, and more than 2,500 expert reviewers. In short, the IPCC reports are humanity’s best attempt to date at getting the science right.

Over the last 800,000 years, Earth’s climate has been cooler than today on average, with a natural cycle between ice ages and warmer interglacial periods. Over the last 10,000 years (since the end of the last ice age) we have lived in a relatively warm period with stable CO2 concentration. Humanity has flourished during this period. Some regional changes have occurred – long-term droughts have taken place in Africa and North America, and the Asian monsoon has changed frequency and intensity – but these have not been part of a consistent global pattern.

The rate of CO2 accumulation due to our emissions in the last 200 years looks very unusual in this context (see chart above). Atmospheric concentrations are now well outside the 800,000-year natural cycle and temperatures would be expected to rise as a result.

Moreover, the IPCC in 1995, in its second assessment report included a sentence that hit the headlines worldwide:

“The balance of evidence suggests a discernible human influence on global climate”

By 2001, IPPC’s third report was even clearer:

“There is an new and stronger evidence that most of the warming observed over the last 50 years is attributable to human activities.”

By 2007, in it’s fourth report, IPCC spoke more strongly still:

“Human induced warming of the climate system is widespread”

In 2013, in the 5th Assessment Report, they stated,

“It is extremely likely that human influence on climate caused more than half of the observed increase in global average surface temperature from 1951 to 2010”

Human activity has led to atmospheric concentrations of carbon dioxide, methane and nitrous oxide that are unprecedented in at least the last 800,000 years.

There is, therefore, a clear distinction to be made between what is “natural variability” and what is our contribution.

“The amount of warming is insignificant…”

The European Geosciences Union published a study in April 2016 that examined the impact of a 1.5°C vs. a 2.0°C (bear in mind we are at 0.8°C now, without the slightest chance of slowing down) temperature increase by the end of the century. It found that the jump from 1.5 – 2°C, a third more of an increase, raises the impact by about that same fraction, on most of the natural phenomena the study covered. Heat waves would last around a third longer, rain storms would be about a third more intense, the increase in sea level would be that much higher and the percentage of tropical coral reefs at risk of severe degradation would be roughly that much greater.

But in other cases, that extra increase in temperature makes things ever more dire. At 1.5°C, the study found that tropical coral reefs stand a chance of adapting and reversing a portion of their die-off in the last half of the century. But at 2°C, the chance of recovery disappears. Tropical corals are virtually wiped out by the turn of the century.

With a 1.5°C rise in temperature, the Mediterranean area is forecast to have about 9% less fresh water available. At 2°C, that water deficit nearly doubles. So does the decrease in wheat and maize harvest in the tropics.

Bottom line: It may look small but it’s a huge deal.

“The benefits will outweigh the problems”

When people talk of alleged benefits of climate change, they are usually talking about agriculture. The argument says that the increased concentrations of CO2 will give a boost to crop harvests leading to larger yields.

This is laughable

Climate change will slow the global yield growth because high temperatures result in shorter growing seasons. Shifting rainfall patterns can also reduce crop yields. Climate trends are already believed to be diminishing global yields of maize and wheat. These symptoms will only worsen as temperatures and extreme weather events become more common. If climate change is allowed to reach a point where the biophysical threshold is exceeded, as would be the case on current emission trajectories, then crop failure will become normal. Also, the severest risks are faced by countries with high existing poverty and dependence on agriculture for livelihoods. Even at “low” levels of warming, vulnerable areas will suffer serious impacts.

Sub-Saharan Africa, according to the World Economic Forum, at 1.5°C warming by 2030 would bring about a 40% loss in maize cropping areas;

South East Asia, in a 2°C would experience unprecedented heat extremes in 60%-70% of their areas.

Agricultural productivity is at risk, not only in developing countries but also in breadbasket regions such as North and South America, the Black Sea and Australia.

Moreover, in October 2015, a study published in Nature estimated that the world could see a 23% drop in global economic output by 2100 due to a changing climate, compared to a world in which climate change is not taking place. The coauthor of the study had this to say,

“Historically, people have considered a 20% decline in global GDP to be a black swan: a low-probability catastrophe – Instead, we’re finding it’s more like the middle-of-the-road forecast.”

“Technology will come to the rescue…”

Deniers who make this case seemingly acknowledge climate change, yet they are optimistic believers in technology being the be-all end-all and that geo-engineering will save us from the clutches of global warming. There are two things I find problematic about this approach:

I think this argument is akin to the “We almost discovered nuclear fusion- we’re only 20 years away!” argument, which stipulates that the nuclear fusion is at any given point in time 20 years away. It takes into account that we have not developed the appropriate technologies to “save” us from climate change, and when we do, there is still a maddening lag between the innovation and deployment. Not to mention the fact we still have not identified which technologies can do the greatest good in the shortest time so we cannot fly blindly in a vague hope that tech will rescue us;

Such an approach fights the “symptoms” of climate change, not the cause of it, meaning that it entrenches our extremely wasteful and inefficient ways that have brought on climate change in the first place.

None of this is to say that I do not believe that technology will play a pivotal role in our transition, of course, it will! But we cannot afford to rely entirely on waiting for carbon capture and storage and the likes to become a deployable and scalable economic reality.

“We shouldn’t wreck the economy to fix the problem when it’s still uncertain!”

When you really get down do it, people will just tell you what their ultimate bottom-line is. If we don’t know with absolute confidence how much you warmer and what the local and regional impact will be perhaps we’d better not committing ourselves to costly reductions in greenhouse gas emissions.

I have written a post on the employment benefits tied to jobs in the renewable energy sector, and there are a plethora of studies pointing to the huge costs of climate change inaction, amongst these, a new study by scholars from the LSE, published last year in Nature Climate Change, offers a daunting scenario.

They estimate that a business-as-usual emissions path would lead to expected warming of 2.5 degrees C by 2100. Under that scenario, banks, pension funds, and investors could sacrifice up to $2.5 trillion in value of stocks, bonds, and other financial assets. The worst-case scenario, with a 1% chance of occurring, would put $24 trillion (about 17 % of global financial assets) at risk. This is but one of the scenarios that have been studied, that point to the huge costs of inaction.

Climate change can affect the economy in myriad ways; including the extent to which people can perform their jobs, how productive they are at work, and the effects of shifting temperatures and precipitation patterns on things like agricultural yields or manufacturing processes. These factors help determine our “economic output” — all the goods and services produced by an economy.

In spite of the fact that there is disagreement on how much exactly economies will be affected, we know the cost of inaction will be immense. With the information at our disposal, it would be foolish and dangerous to assume that reducing emissions will cost more than coping with a changing climate.

Good luck with your “debate” and let me know how it goes.

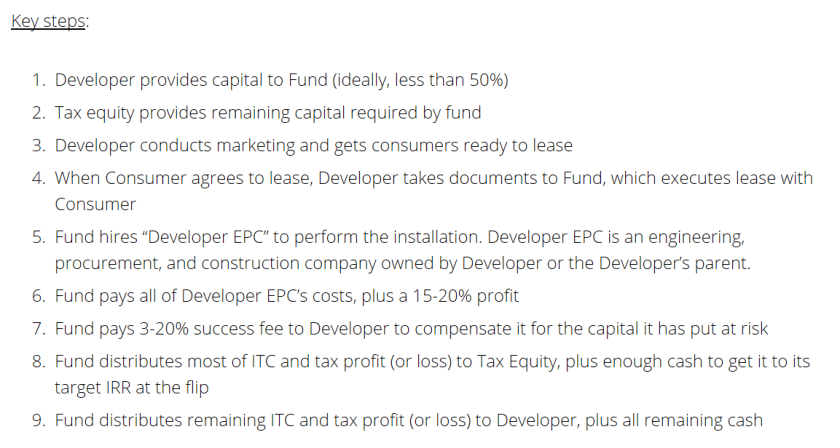

There is quite a bit of confusion regarding what tax equity is for renewable energy and how it can be taken advantage of. This is largely because tax equity structures are ubiquitously understood to be complicated, meaning many firms just don’t bother with them. That’s a mistake. Tax equity can be a powerful incentive for developing RE in the USA.

Companies that have managed navigate the system have been able to reap the benefits of tax equity structures, but new entrants can be deterred, therefore bypassing potential benefits.

What is Tax Equity?

Tax equity is where renewable energy and tax policy intersect.Basically, tax equity is a creative and complex way to split the benefits of installing and producing RE electricity from their corresponding tax benefits.

Tax credits, however, can only be used by clean energy developers who are profitable enough to pay larger amounts of taxes. Because of this, many smaller players, who are not very profitable cannot reap the benefits of tax credits. Hence, they must find an investment partner with enough income to be able to reap credible benefits from tax credits.

Installing renewable energy is subsidized by a tax credit. This means that a solar project developer/company/host wants to have the benefits of solar electricity production (via decreased utility bills) but does not the tax liability to use the tax credits, so it passes those credits to an investor who in return puts up capital to pay for the solar project. The objective is to reduce its own tax bill by receiving the tax deduction. Tax equity financing is primarily provided by large banks, insurers or big corporations which provide upfront investment in exchange for tax credits associated with the development of (usually) solar energy projects.

Example:

Take solar developer start-up, Sunny Ltd., who wants to develop a large solar PV project. The cost of the project would be $1m. Although such an investment in RE carries corresponding tax credits, Sunny Ltd. is currently not profitable enough to take advantage of them, so they decide to rope in a Tax Equity Investor. The Tax Equity Investor, represented by Capital One Bank, wants to apply the tax credits to their own corporate tax bill.

So Capital One Bank can put up, say 40% of the solar project financing, used as equity (the remaining 60% hypothetically will come from debt).

So if the bank puts up $400K in equity, they could hypothetically reduce their tax bill by a certain amount over the course of a contract.

State of the Market

According to specialized law firm Chadbourne & Park, the market is steadily increasing. The U.S wind and solar markets in 2015 saw $11.5 billion in new tax equity deals, up from $10.1b from the year before. According to John Eber, head of energy investments at J.P Morgan, of that 11.5b, $6.4b was secured in the wind marketplace for projects totaling 5,700 megawatts capacity. There was three main sponsors int he winds tax equity investors that completed deals totaling $1b each (47% of tax equity raised in 2015).

In the solar residential tax equity market, about $2.6b was raised by three leading residential solar companies, accounting for 90% of the residential market, (up from $1.9b in 2014). Eber went on to say that distributed generation and utility-scale solar marketplace accounted for an additional $2.5b in tax equity deals. Eber says there are about 20 active tax equity investors in the wind marketplace and 27 in solar, with some crossover, and of the 20 active investors in wind, 17 entered into deals in 2015.

The small number of players is attributed, in part to the complex nature of tax equity and the associated costs and in part due to the fact that tax equity investors must have very large tax liabilities, to justify such operations.

But be that as it may, it is still a huge increase if you consider that after the financial crisis, the number of Tax Equity Investors collapsed from 14 providers to just 5 (Jacoby, University of Pennsylvania Law Review), since in order to take advantage of tax equity, you need to have huge tax liabilities and the after 2008 fewer companies had the necessary tax liabilities to make tax credits attractive.

Before we have a look at a few tax equity structures used, bear in mind who the stakeholders are:

Tax Equity Agreements usually have three stakeholders, although sometimes the developer and host are the same:

A Developer (ex. a solar PV installer like SolarCity or FirstSolar ) who identifies a potential solar project and decides to undertake the costs and risks of engineering, procurement, installation, and commissioning;

The Solar Host who is usually either a residential or commercial building owner, and is interested in the benefits of solar power;

A Tax Equity Investor who usually is an institution like a bank or a corporation like Google, that has to have two things:

high tax liabilities, or at least high enough to make a tax credit attractive

the liquidity necessary to undertake the development of a solar project.

The Tax Equity Investor has to agree to finance and own the project for a number of years and in return for undertaking the construction and ownership costs of the solar project the company will receive the corresponding tax deductions.

The Tax Equity Investor is the defacto owner of the physical solar panels, while the benefits go to the host, and once the Tax Equity Investor reaps in the desired returns brought by the tax credits associated with the solar projects they return ownership to the developer.

Tax credit structures can vary quite a bit, but here are the two most common types:

The Partnership Flip

As you can probably imagine, a Tax Equity Investor does not necessarily want to hang on to the solar panels for the entire life of the project- why would they? Enter The Partnership Flip. This is where the ownership of a project is owned byboth developer and tax equity investor but in varying degrees.

Source: Woodlawn Associates

The Tax Equity Investor and the developed enter into a partnership in which the have joint ownership of the solar project. Say, at the beginning of the project the ownership the Tax Equity Investor will hold 90% while and the developer will own 10%. Progressively, as the Tax Equity Investor begins to reap the rewards of the tax credits, the ownership of the project will begin to “flip”, whereby the Tax Equity Investor will own 60% and the Developer 40%…then 50%-50% until it is 10%-90% for the Developer.

Sale – Leaseback Agreement

Source: Woodlawn Associates

This agreement sees the solar developer selling the project to the tax equity investor and then the tax equity investor leases it back to the solar developer. It’s actually simpler than a partnership, because all the tax benefits pass directly to the tax equity invest right away, whereas with a partnership, years pass before the Tax Equity Investor reaps all the benefits.

The Developer will install, operate and maintain the project and a Host will agree to purchase the power generated from the project, via a PPA.

The Investor keeps all the tax benefits and receives payment (cash) in the form of rent from the solar developer. The developer’s revenue from the PPA is used to make rental payments under the lease. The developer has a taxable gain on the sale of the project to the extent that the value of the project exceed the cost to build it. Indeed, the developer will usually have the option, exercisable at the end of the lease period, to buy the project from the investor at its fair market value.

The developer and the tax equity investor are like to two passengers in a car, when the car hits a bump, they are both impacted.

With solar and wind installations predicted to increase, 2017 will definitely see more tax equity deals for renewable energy, but what remains to be seen is if investors will be able to keep and meet the capital requirements of the industry.

There is a famous quote by Former Saudi Oil Minister from 1962-86 Sheik Zaik Yamani that people in (renewable) energy never tire of throwing out there,

“The Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil” – Sheik Zaik Yamani

Sheik Yamani was no wishful thinker.

Energy shifts happen, in part because of poles pulling in different directions, not necessarily because of a lack of supply. There is plenty of oil in the ground and it is being extracted more cheaply and efficiently than ever before, yet the current environment is propelling Saudi Arabia (&Co) into the opposite direction.

Today, when someone mentions Saudi Arabia’s energy mix, what usually comes to mind is crude, crude and more crude, but come a few years this will change radically. With the nosedive that the oil price took in the last few years, Saudi Arabia is launching a massive renewable energy plan to try to replace some, if not all, of their energy needs.

The Plan

Newly appointed energy Minister Khalid al-Falih, a graduate of Texas A&M University and Chairman of Aramco, intends to launch an ambitious renewable energy program and is currently soliciting tendering bids. The program, which is to be officially launched “very soon” is expected to involve an investment of between $30 billion and $50 billion by 2023, he said at a press conference in Dubai.

Minister al-Falih interviewed by CNN’s Becky Anderson @ ADSW 2017, Solarpv.tv

The plan involves the development of almost 10 gigawatts of renewable energy by 2023, starting with wind and solar plants across the sun-soaked northwestern desert. The effort has the potential to replace the equivalent of 80k barrels of oil a day now burned for electricity generation.

According to Bloomberg, bidders seeking to qualify to build 700 megawatts of wind and solar power plants should submit documents by March 20, and those selected will be announced by April 10, Saudi Arabia’s energy ministry said Monday in an e-mailed statement. Qualified bidders will be able to present their offers for the projects starting on April 17 through July.

The Kingdom intends to require all investors to invest in the local supply chain of goods and services, so as to render themselves more competitive.

🇸🇦The Kingdom’s Electricity Needs

Relying heavily on hydrocarbons as feedstock for the electricity sector, Saudi Arabia is by far the largest user of crude oil for power generation in the world. Oil accounts for two-thirds of the input into electricity generation, with natural gas providing most of the remaining portion, according to the Joint Organizations Data Initiative (JODI). During the prohibitively hot summer months, consumption of electricity increases as domestic demand for air conditioning rises. The Kingdom has recognized that this is both highly inefficient, expensive and unsustainable.

EIA, JODI

Saudi Arabia used an average of 0.7 million bbl/d of crude oil for power generation during the summers from 2009 to 2013, which is massive. To put this into perspective, that same period, Iraq and Kuwait, the next two largest users of crude oil for power generation in the Middle East, each averaged roughly 0.08 million bbl/d of crude burn. At the same time, net electricity consumption in Saudi Arabia has more than doubled since 2000.

Shifting the energy mix towards renewable energy would bring about several key advantages:

Local Emissions Reductions: more on that later;

Economics: The Kingdom has seen two years of budget deficit, and is looking at a $53b deficit moving into 2017. Stubbornly low oil prices have forced austerity measures on a country that is not associated with belt- tightening measures. In the context of the 2018 Aramco IPO prospected to raise $100b, it is clear that the economic tide is shifting. With the Kingdom’s main sources of income: oil exports, decreasing due to a number of economic factors, this leaves less for exporting and therefore less revenue. By shifting to renewables, they aim to free the crude currently being consumed domestically so they can export it, thus generating more revenue;

Diversification: diversifying their investment portfolio away from oil is recognition that an economy based on the export of crude is, as demonstrated, highly vulnerable to prices drops and other external shocks.

Price Oil Drop from 2014- Feb 2017

Saudi Arabia has boosted output for years to sustain export income while also satisfying domestic demand. Demand for refined fuels such as gasoline has doubled since 2003, according to JODI. Moreover, Saudi Arabia, the UAE, Qatar, Oman, and Bahrain have significantly reduced or eliminated fuel subsidies over the past year to limit government spending because of low oil prices. Brent crude is trading at $55 a barrel today compared to $112 per barrel between 2011 and 2014.

Domestic demand for oil increased by about 24,000 barrels a day in the first five months of 2016, the slowest growth rate for that period since at least 2010, the first year according to JODI.

Bloomberg, 2016

Mario Maratheftis, chief economist at Standard Chartered Plc. said, according to Bloomberg, “Renewable energy is not a luxury anymore – If domestic use continues like this, eventually the Saudis won’t have spare oil to export.’’

Without alternative power sources, including gas and renewables, the kingdom would be forced to increase the amount of crude it burns, diverting it from exports. That can reach as high as 900,000 barrels a day during the kingdom’s summer months, according to data from the JODI.

Saudi Arabia has already taken steps to substitute natural gas for oil in power plants, a change that’s had “immense” impact on the crude burn, OPEC said in its Monthly Oil Market Report released in January. The use of crude for domestic power has fallen by nearly 1/3rd since the Wasit gas plant began operations in March 2016, according to the OPEC report.

300,000 Barrels

Saudi Aramco will bring online the similar-sized Fadhili gas project in the country’s east by the end of the decade. That gas project along with the renewable projects, planned for completion by 2023 could save about 300k barrels of oil from being burnt for power, according to estimates based on IEA and OPEC data.

According to Fabio Scacciavillani, chief economist at the Oman Investment Fund, “Alternative energies are a key factor in the economic transformation, this region has a great competitive advantage in low-cost energy production and that will continue with renewables. That will create a big advantage particularly in energy-intensive industries.’’

On top of that, the Saudis want to build nuclear reactors, a less ambitious program that would see 2.8 GW of new electric capacity.

The end goal is to generate 30% of the Kingdom’s electricity from renewable sources by 2030, with the remainder to come from natural gas and a small portion from nuclear.

Deputy Crown Prince Mohammed, at the forefront of promoting reforms and development in his country, said, “I think by 2020, if oil stops, we can survive…We need it, we need it, but I think in 2020 we can live without oil.”

The Tide is Turning to an Energy Transition

It goes without saying that the primary reason the Saudis are shifting to renewables is economics rather than emissions, yet we can still predict some emission reductions.

It is clear that the Kingdom does not expect oil prices to increase above $100 like it was a few years ago. They know that the days when they would squeeze massive economic rent out of oil have passed. Their long-term objective is to ensure the future competitiveness of their oil in a global environment where paradoxically, fossil fuels are abundant and renewable energy has a higher penetration, while still decarbonizing their energy sector.

This takes me back to Sheik Yamani’s prediction. It is not so much that the Kingdom is physically running out of oil to sell as much as the energy environment is changing. The supply is outpacing demand and oil is just not as profitable as it was. The hammer blows of energy efficiency, renewable energy, and global economic trends are forcing a transition to better options.

“The [traditional] energy system employs millions of people!”

“Renewables will create massive job losses!”

“Fossil fuels may not be good for the planet, but at least they employ millions!”

and last but not least:

“Green jobs are the miracle that never happened”

Far be it for me to assess whether green jobs were ever meant to be “miraculous”, but I will say that “green jobs”, defined by the US Bureau of Labor Statistics (BLS) as either “jobs in business that produce goods and services that benefit the environment or conserve natural resources” or as “jobs in which workers’ duties involve making their company’s production process more environmentally friendly or use fewer natural resources”, are increasing at unprecedented levels.

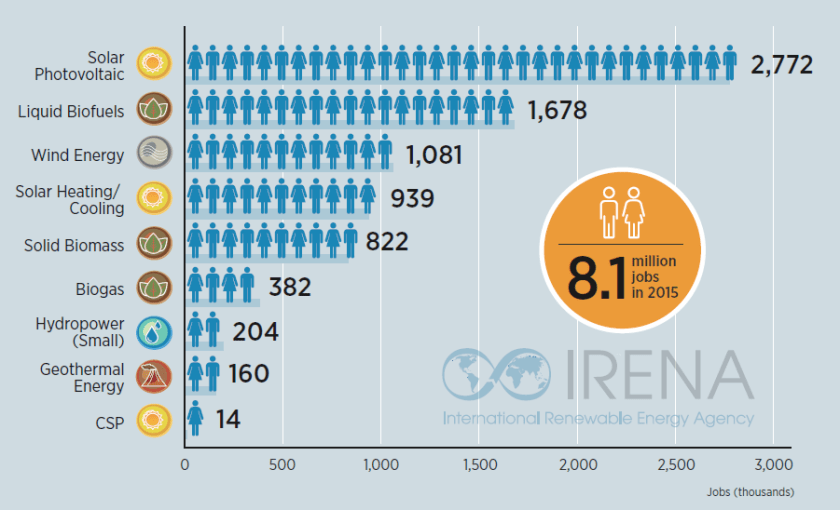

Number of Jobs in Renewably Energy, Irena, 2016

The International Renewable Energy Agency (IRENA) published their annual report detailing employment in the IRENA’s 2016 report, (link here – to learn more about their methodology, I suggest you check it out) estimated total employment in the RE sector to amount to 8.1m people. Adnan Amin, director-general or IRENA commented on the report stating, “The continued job growth in the renewable energy sector is significant because it is in contrast to trends across the energy sector. The increase is being driven by declining RE technology costs and enabling policy frameworks.”

Most of these jobs are in China, Brazil, USA, India, Japan, Germany, Indonesia, France, Bangladesh, and Colombia.

Renewable Energy Jobs by Country, Irena, 2016

Jobs in renewable energy increased by 18% from the estimates reported two years ago with a steady regional shift towards Asia.

In 2014, the Solar PV emerged as the largest employer in the energy sector accounting for 2.8 million jobs, an 11% increase from last year, and two-thirds of which were in China. Solar PV grew the most in USA and Japan while decreasing in Europe. Indeed, the global aggregate production of solar panels keeps increasing and pushing further into Asia, with lower costs of installations driving that accelerated growth. Global wind employment crossed the 1m job mark, fueled mainly by deployment in China, Germany, the USA, and Brazil.

Although, it’s good news (mostly) all around, the winner this year is:

🇨🇳Gold Medal: China

China has firmed up to be the leading renewable energy job market in the world, with 3.5m people employed. Domestic deployment and rising solar PV demand solidified that growth at 4% to 1.4m jobs. Chinese Solar PV jobs are focused on manufacturing (with 80%) following by installations and operations. The largest solar water heating technology industry and market are in China since they provide for both domestic and international demand. Half of the global wind jobs are in China, and more than 70% of those are in manufacturing.

Moreover, China is also is a leader in hydropower employment, as they add 75 GW of new projects between 2014-2017. Construction and installation account for 70% of the countries large hydropower employment.

Indeed, China has and installed 65 gigawatts more in renewable energy in 2015, shift the labor force from oil and gas, towards renewables. Now, China employs 3.5m people in renewable energy and only 2.6m in oil and gas, that 35% more people in RE than in oil and gas (coal excluded).

Source: Irena, taken from Bloomberg

Although the lion’s share of the RE labor force is employed in manufacturing, this growth rate is likely to begin to contract, in spite of growth in technological deployment due to:

market consolidation in favor of large suppliers/ manufacturers resulting in economies of scale;

automation of process will make manufacturing more efficient, which will make it less labor intensive.

The runner up is:

🇺🇸Silver Medal: United States

Renewable energy jobs in the USA have increased at a historic pace, owing to large consumer demand and constantly declining prices of RE, especially solar. The Solar Foundation’s National Solar Jobs Census 2016 found that the solar industry accounts for 2% of all jobs created in the US over the past year, with the absolute number of solar jobs increasing in 44 of the 50 states. As of November 2016, there were 260k solar workers employed in America, “representing a growth rate of 24.5% relative to November 2015” according to the report.

This is great news all round since it signals that solar is receiving investments and creating thousands of high-skilled jobs, ultimately driving growth, strengthening businesses and reducing emissions (pollution) in cities. Moreover, wind recovered from a policy-induced slump in new installations and saw wind jobs rise by 43%.

Moreover, according to the annual U.S Energy Employment Report, published January 2017, more people are employed in solar power last year than in coal, gas, and oil combined. They report found that 43% of the total electric power generation workforce was employed in solar energy while fossil fuels accounted for a mere 22%. The report goes on to say that the US solar installation sector alone employs more than the domestic coal industry. Since 2014, solar installation has created more jobs than oil and gas pipeline construction and crude petroleum and natural gas extraction combined.

Source: Department of Energy, BLS, taken from Bloomberg

The electricity mix in the USA is shifting decisively in the direction of renewable energy, driven by the transition from coal-fired power plants, to gas and now, steadily in low-carbon energy sources.

🇧🇷Bronze Medal: Brazil Employment in RE in Brazil is concentrated in the cultivation and production of biofuels. I am aware that there is a huge debate regarding whether of not biofuels production (especially from sugarcane..etc) is considered a real “green job” but that is an argument for another day, but today, I will be counting them as green jobs.

With 821,000 jobs, Brazil continues to have the largest liquid biofuel workforce by far. Reductions of about 45,000 jobs in the country’s ethanol industry (due to the ongoing mechanization of sugarcane harvesting, even as production rose) were only partially offset by job growth in biodiesel. Biofuel production, especially in a developing country tends to be labor intensive, on account of inefficiency and poor access to technology, which have explained why those working in biofuels in Brazil are just under 1m people.

However, Brazils wind energy sector is growing rapidly, which power capacity expanding from 1 GW in 2010 to 6 GW in 2014. Moreover, while there was one mere wind power equipment manufacturer, there were ten in 2007, indicating the sector is maturing. Most of these jobs are in construction and manufacturing.

Brazil’s solar heating market is expanding strongly in the past decade. In 2013, there were an estimated 41k people employed, between manufacturing and installation.

🇪🇺Consolation prize: European Union

Owing to a mélange of adverse policy conditions, regulatory uncertainty and a sharp decrease in investment, the number of RE jobs in the EU declined from 1.25m to 1.2m. Germany, however, is the euro leader in terms of job, with 271k jobs in RE. This is more than double the runner-up, France, which is ahead of UK, Italy, and Spain. RE employment in France fell by 4%- primarily because solar PV installations dwindled by 45%). We are likely to see a shift, due to Denmark and the UK’s ambitious off-shore wind plans which will (if they go through with them) likely create expansion in the near future. The EU has been suffering consistent defeats against China in terms of lower manufacturing competitiveness and a weaker installations market, leading to a net decrease in solar jobs… for now.

“But Jobs!”

Growing awareness of the harmful effects of GHGs on the environment and on our health, coupled with consumer preferences are pushing investment into renewable energy, leading to logical increases in employment in RE. Conversely, the tumbling price of oil has led to a slowdown of industry expansion (too expensive deep off-shore, arctic projects, and unconventional drilling) and the corresponding reduction in capital expenditure and operational expenditure has had significant effects on the oil and gas labor force.

I do not think that the “But what about the jobs!” argument to be complete without merit. But a growing trend and body of evidence point to the fact that potential job losses in the traditional energy sector can be compensated by green jobs, however, an argument runs in parallel with this reasoning. And that is the fact that energy jobs are geographically and personally specific, meaning you can’t plug a worker out of an oil field in Texas and jettison them into a solar PV role easily. Re-skilling, training, and compensation for job losses are some of the conversations we will have to have in the next few years.

Happy New Year to everyone, thank you for your e-mails!

I wanted to run you through what articles I am working on at the moment, feel free to chime in at any time if there is something you would prefer to read about ⚡️

How to Handle a Climate Change Skeptic – You guys are requesting this, so I will definitely write about it, although I admit I really resent having to add my two cents on how to handle people who categorically reject fact based evidence;

Solar Securitization – Due to the rise of third-party leasing and Power Purchase Agreement (PPA) models, whereby energy clients can enter long-term developers that install, own and operate solar equipment on their roofs. In return, the host customer pays the developer for the solar system’s electric output, similar to how they would pay a utility for their services. These models lend themselves to the securitization of solar assets, a financing technique that puts together pools of underlying assets and transforms the future cash flows into a security. Once the risks are elaborated and understood, there would be many benefits for all parties;

The Tyranny of Short Termism – There are so many things to say on this topic, on the one hand, a greater long-term focus, a growing body of empirical evidence pointing to, companies’ financial performance becoming more predictable, read: more profitable3. If your focus on profit is sufficiently long, it starts to become more and more genuine representative of the long-term benefits and costs. But there is a growing appreciation of the massive economic threats posed by climate change, the ultimate long-term risk;

Insurance and Climate Change – The $600 billion reinsurance (insurance for insurance companies-yes, it’s a thing) industry helps insurance companies pay damage claims from hurricanes and floods and can help people and companies get back on their feet after disasters, which are getting more frequent, and deadly on account of climate change. Swiss Re data shows natural disasters caused an average $180 billion in economic damage per year over the last10 years, of which 70% was uninsured. I wanted to look at these numbers and explore why insuring climate change was is challenging;

Macquarie’s purchase of the Green Investment Bank – Aussie investment bank Macquarie closed a 2b deal to privatize the UK government backed Green Investment Bank. This will lead to interesting developments fo UK green infrastructure;

An overview of the feasibility of the biofuel industry

Also, I realize that I am not as active as I ought to be, and I promise you, I will publish more regularly!

Innovation and tech breakthroughs are key drivers of the renewable energy (RE) and clean tech sectors, and in this regard, venture capital (VC) has a powerful grip on the imagination. Indeed, some of the biggest names in tech, like Amazon, Google and Uber are around today thanks to VCs. This has led many to wonder, where are the big, ubiquitous clean tech start-ups that made it big?

Except it’s not as simple as that, collective imagination romanticizes VC, but it is important to separate the myth from the reality and understand that the RE sector is categorically different from IT and tech, and that VC does not lend itself well to the clean tech.

A bit of backstory first: Boom and Bust cycles

In 2005, VC investment in clean tech was in the hundreds of millions. The following year, it increased to $1.75b, according to the National Venture Capital Association. By 2008, investment had skyrocketed to $4.1b (see figure 1). And the US government followed the trend, eager to continue to develop the meteoric rise of promising innovative technologies through a mix of loans, subsidies, and tax breaks. They directed $44.5b into the sector between 2009 and 2011. In other words, the cleantech sector was in full throttle and VCs thought it was ripe for disruption.

Gaddy, Sivaran & O’Sullivan, MIT Working Paper, 2016

But then, due to a confluence of unfavourable events, including:

Fluctuating silicon prices: According to a GTM Research report, high purity silicon (polysilicon), the principal material for solar panels played only a minor role in this price collapse, as over 80% of polysilicon is sold via long-term contracts, and the pricing on these contracts moved little for most of 2011. However, the oversupply in the polysilicon market shifted the spot price of silicon down from $80 per kilogram in late March 2011 to under $30 per kilogram in December, which resulted in a 60% price drop. This lower spot price gave silicon customers the leverage to renegotiate contract pricing downward, and this resulted in much lower realized silicon average selling prices (ASPs) moving forward;

Newly cheapened natural gas (shale boom): Since gas has got so cheap, there was no longer a financial incentive to go with renewables. Technical breakthroughs in natural gas extraction from shale, namely fracking—have opened up reserves so massive that the US has surpassed Russia as the world’s largest natural gas supplier. Because 24% of electricity comes from power plants that run on natural gas, that has kept downward pressure on cost to just 10 cents per kilowatt-hour, and producing significantly less than half the CO2 pollution of coal at that. This new environment made investors divert capital from RE into natural gas;

The 2008 financial crisis: A large proportion of the gains VC firms had made between 2003 and 2007 disappeared, and the sudden and unexpected lack of capital, coupled with the difficulty of taking smaller companies public, hit renewable startups particularly badly. Venture investments in clean tech fell from $4.1 billion in 2008 to $2.5 billion in 2009, which made it difficult to raise money to achieve manufacturing scale;

China’s high paced production of solar infrastructure: Globally increasing demand for solar infrastructure combined with a domestic push on solar manufacturing had propelled China to the top position in terms of PV manufacturing countries. Indeed, since 2004, China’s meteoric production on all fronts of the solar manufacturing value chain, beginning with polysilicon feedstock, to wafers, to cells and modules. By 2008, the ascent of solar industry became so formidable that Chinese firms started reaping economies of scale in the production of purified silicon. By then, China had become the largest PV manufacturer in the world, with 98% of its product shipped overseas.

The clean-tech bubble had burst and the euphoric VC investments came to a swift close. Moreover, shares of public clean tech firms traded at steep discounts to the market peak in 2008, and almost all of the 150 renewable energy start-ups founded in Silicon Valley over the past decade had shut down or were on their last legs. The fallout sent ripples through to every niche in the clean-tech sector: wind, biofuels, electric vehicles, fuel cells and especially solar.

The most prominent casualty of this financial carnage was Solyndra, a start-up designing and manufacturing cylindrical solar tubes, which had received $500 million in federal loan guarantees but after the price of polysilicon crashed they were forced to file for bankruptcy.

The Venture Capital Model: How it works

In a nutshell, VC funds are usually structured as 10-year “partnerships”, where external investors (the limited partners, or LPs) provide capital to the VC fund (run by the experienced general partners, or GPs) to make investments on their behalf. The Model is summed up nicely below.

Zider, Harvard Business Review, 1998

VC investment usually goes like this:

Part 1: A fund will tend to invest in a portfolio of 10-20 start-ups over the first 5 years and harvest the returns in the remaining 5 years.

Part 2: Ideally, sizable returns begin to materialize when a portfolio company is acquired by another firm or when it issues shares on a public market through an initial public offering (IPO)—these events are known as “exits.”

VC funds also tend to invest at several stages of a company’s development, starting with early “seed” rounds, typically $1 million or less, continuing through the next rounds (known as “A”, “B”, “C” rounds). The objective of the VC is to exit and get your returns, but if a company cannot exit within three to five years of raising a major funding round, the VC is likely to write off the investment.

Bear in mind that VCs have contractual investment structures that limit their scope. Take a company that doubles its revenues every year for 20 years, and expands from thousands in revenue to billions, a VC would most likely not touch it, because a VC could not wait 20 years because their funds are could be structured with a requirement to earn returns every 10 years. VC are extremely impatient.

The point of VC is, in theory, to invest in the balance sheet and infrastructure of a company until it reaches sufficient size and credibility so that it can be acquired by a competitor or so that the institutional public-equity markets can step in and provide liquidity. The venture capitalist is, essentially, buyinga cut of someone’s idea, nurturing it for a short period of time so that it becomes profitable, the with the help of an investment bank, exiting.As long as venture capitalists can exit the company, before the company’s’ value ceases rising, they can reap huge returns at a relatively low risk. Indeed, really good VCs operate in “secure” niche environments, where they know the industry inside out, and where traditional low-cost financing is unavailable.

What is a VC’s target investment?

Now, I know, you can point to Tesla, or Boston-Power Inc, a lithium ion battery provider or Sunnova Energy Corp, a provider of residential solar systems, that both raised $250m from VCs, and I agree, there are also many success stories.

In 2014, according to the National Venture Capital Association, the sector as a whole raked in $2b, which is a 41% increase relative to 2013, but it is a 30% decrease compare to 2012. The absolute number of clean tech deals is also up, suggesting that VC are being much more judicious with their investments.

Classically, sectors such as IT and software are ideal recipients of VC. According to Ghosh and Nanda from Harvard, (for more info, check out Ghosh & Nanda, Venture Capital Investment in the Clean Energy Sector. Harvard Business School Working Paper. doi:10.2139/ssrn.1669445), this is mainly due to:

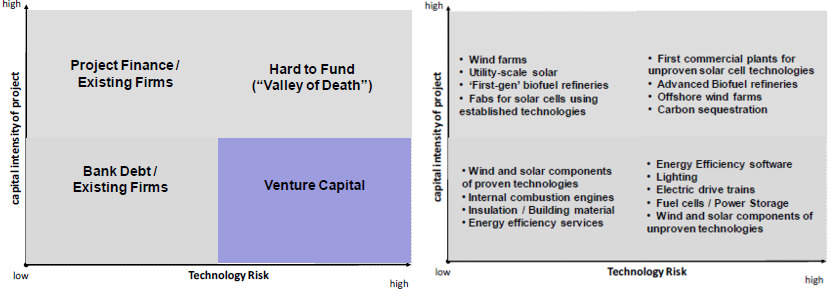

1. Lower levels of capital intensity are highly desirable for VC investors. As you can see in the figure below, the “sweet spot” for VC is typified by high technology risk, but low capital intensity, where a syndicate (a group) of two or three banks can completely fund a start-up through to its IPO.The ability to reduce risk capital and quickly access infrastructure capital is a key differentiator between the IT sector andRE start-up. RE technologies are usually large-scale systems with sizeable physical footprints. They are costly to not only to build but also to operate and maintain. Making a company on the supply side of the energy business requires a serious investment on the industrial side that the VC firms didn’t fully reckon with.

Ghosh & Nanda, Harvard, 2010

2. IT companies have appropriately shorter sales cycles meaning that their products are commercialized promptly, ultimately meaning that VC can exit faster. The textbook example here is Google, that had an IPO 5 years after it received its first round of VC funding and having raised roughly $40m (!) in VC. As many VCs found out the hard way, energy companies don’t operate on those timelines. Consider this analysis by Matthew Nordan, a venture capitalist who specializes in energy and environmental tech. Of all the energy startups that received their first VC funds between 1995 and 2007, only 1.8% gained what he calls the end goal of a VC, meaning an initial public offering on a major exchange.

3. Whilst IT companies face incumbents with high-cost structures, clean energy companies face incumbents like ENI, Shell, and Exxon, who actually have lower cost structures owingto the fact they are giant, well-financed, often more than a century old and established, propped up by diversified investments. And, yes, of course, the average IT company requires infrastructure investment, but it is on a whole other level relative to RE infrastructure, which requires an entire host of investments ranging from diffusors, chillers, arrays and transmission lines,all of which must be manufactured, shipped and installed. It boils down to the fact that an RE company cannot scale and grow as quickly as an IT comply, delaying a potential exit for the VC.

None of this is to say that VC does not have value for RE, it does! VC are often the only private money willing to take the risk of investing in cutting-edge companies, but that’s their niche. Remember that the venture capital niche exists because of the structure and environment of capital markets. Someone with an idea or a new technology often has no other source of financing to turn to. Banks will only finance a new company to the extent to which are hard assets against which to secure the debt, and renewable energy companies and clean tech actually do have hard assets.

tl:dr Renewable energy companies have capital requirements, growth profiles and competitive environments that do not make them ideal candidates for VCs.

Old critiques, die hard. For the longest time, renewable energy (RE) has been viewed as too expensive and un-scalable, as a luxury energy source, that will not be deployed in developing countries. As a matter of fact, how many times did you hear the criticism, that by diverting investment away from so-called “cheap” fossil fuel energy, we would be depriving developing countries of their right to develop?

The numbers quantifying investments in RE are in! It should be no surprise that RE investment is increasing significantly and the developing world, especially China, is leading the way.

The findings of the United Nations Environment Programme (UNEP) Global Trends in Renewable Energy Investments 2016 confirmed that RE set new records in 2015 for dollar investments, the amount of new capacity added and the relative importance of developing countries in the context of that growth.

Record-breaking uptrend in Renewable Energy Investments

Global investment in RE rose 5% to $285.9 billion from 2014 to 2015, breaking the previous record of $278.5 billion reached in 2011 (FYI that’s double the dollar allocations to new coal and gas generation, which was an estimated $130 billion in 2015) when the famous ‘green stimulus’ programs in German and Italian were in full throttle. The figure below shows that the 2015 investment increased sixfold since 2004 and that investment in RE has not been below $230b since 2010.

GLOBAL NEW INVESTMENT IN RE BY ASSET CLASS, 2004-2015, $BN

Source: UNEP, Bloomberg New Energy Finance

*Asset finance volume adjusts for re-invested equity. Total values include estimates for undisclosed deals.

Over the course of the 12 years shown in the chart, the cumulative RE investment has reached $2.3 trillion.

Moreover, in 2015 some 134GW of RE excluding large hydro were commissioned, equivalent to some 53.6% of all power generation capacity completed in that year – and this is worth mentioning because it is the first time it has represented a majority. Of the renewables total, wind accounted for 62GW installed, and solar photovoltaics 56GW, highest ever figure and sharply up from their 2014 additions of 49GW and 45GW respectively.

Developing Countries Leading the Way

The investment which led to record-breaking levels came from China, which lifted its investment by 17% to $102.9 billion, about 36% of the global total. In the Middle East and Africa, investment was up a total of 58% at $12.5 billion, helped by project development in especially in South Africa and Morocco; and in India, up 22% at $10.2 billion.

More significantly, 2015 was the first year in which investment in RE (excluding large hydro) was higher in developing economies than in developed countries. The figure below shows that the developing world invested $156 billion last year, some 19% up on 2014 and a remarkable 17 times the equivalent figure for 2004, of $9 billion.

INVESTMENT IN RE: DEVELOPED/ DEVELOPING COUNTRIES, 2004-2015, $BN

source: UNEP, Bloomberg

The key contributors to this shift from developed to developing are the big three: China, India, and Brazil, who saw an investment rise of 16% to $120.2 billion

A large part of the record-breaking investment in developing countries took place in China. Indeed China has been the single biggest reason for the strong increasing trend for the developing world as a whole since 2004. In spite of low market fundamentals and much talk of decreased investment in RE, China has been a key contributor to these figures. China invested $102.9 billion in 2015, up 17%, representing well over a third of the global total.

Likewise, India enjoyed a second successive year of increasing investment, breaching the $10 billion for the first time since 2011.

Other developing countries, excluding the big three, lifted their investment by 30% last year to an all-time high of $36 billion, some 12x their 2004 investment, the biggest players are:

South Africa also deserves an honorable mention as it’s RE investment is up 329% at $4.5 billion significantly ramping up their solar PV, in the context of their auction program. In June last year, the government in Pretoria launched a tender for an additional 1.8GW for its renewables program. One of the signal deals later in the year was the financing in September of the 100MW Redstone solar thermal project for an estimated $756m, helped by loans from the World Bank’s International Finance Corporation and Overseas Private Investment Corporation of the US;

Mexico saw a 105% increase at $4 billion, aided by investment from the development bank Nafin for 9 wind projects. Moreover, Mexico is emerging as an important location for bond issues to back renewable energy projects. In November last year, National Financiera issued $500 million worth of five-year bonds to contribute towards the development of nine wind farms with a total capacity of 1.6GW;

Chile saw an increase of 151% higher at $3.4 billion, thanks to a sizable uptrend in solar project financings;

Morocco, Turkey, and Uruguay also saw investment increases in excess of the $1 billion milestone in 2015.

Developed world downward trend (mostly)

In the developed world, however, we are witnessing a downward trend quite consistently, since 2011, when it peaked at $191 billion, some 47% higher than the 2015 outturn. Developed countries invested $130 billion in 2015, down 8% and their lowest figure since 2009. This decline is due to two major factors:

because of the US, where firstly; there was a rush of investment in 2011 as projects and companies tried to catch the Treasury grant and Federal Loan Guarantee programmes before they expired and secondly, the US Supreme Court’s decision in February 2016 to allow all legal objections to the Environmental Protection Agency’s Clean Power Plan to be heard before it can be implemented may be deterring investment in 2016.

but much more to do with Europe, where allocations fell by 60% between 2011 and 2015. That big drop was caused by a mix of factors including retroactive cuts in support for existing projects in Spain, Romania and several other countries, an economic downturn in southern Europe that made electricity bills more of a political hot potato, the cut of government subsidies aimed at incentivizing RE in Germany and Italy, and the big fall in the cost of PV panels over recent years.Italy, in particular, saw renewable energy investment of just under $1 billion, down 21% on 2014 and far below the peak of $31.7 billion seen during the PV boom of 2011.

Retroactive cuts to feed-in tariffs really weaken support for solar energy investments. Spain, scene of particularly painful retroactive revenue cuts imposed by the government during the 2011-14 period, and the end of all support for new projects, saw investments of just $573 million in 2014. This was slightly up on the previous year but miles below the $23.6 billion peak of 2008.

But it’s not all bad in Europe, especially since the UK has not seen a significant slowdown in RE investments in recent years, and is actually pushing in the opposite direction. Moreover, in spite of the fact that offshore wind in the North Sea has seen massive investments amounting to $17b, Europe’s aggregate RE investment is still in decline.

Following several rounds of consolidations by their competitors in the energy sector including General Electric’s purchase of Alstom’s energy business and a merger between Germany’s Nordex and Spanish rival Acciona Wind Power, Siemens and Gamesa have announced their merger.

Siemens and Spain’s Gamesa agreed last week to merge to create the world’s biggest manufacturer of wind farms, with the German company paying 1 billion euros ($1.13 billion) for a majority stake in the combined business. The combined group’s order portfolio would be worth some 20b euros. The merged business will have 21,000 employees, an installed power base of 69 gigawatts.

Before the merger

Before their merger, Siemens had an 8% share of the global wind turbine market, according to data from FTI Consulting, which made it the second-biggest manufacturer after Denmark’s Vestas, which had a share of nearly 12%.

But Gamesa’s relatively small 4.5% market share put it steadily behind other large players, such as China’s Goldwind, which has been growing internationally into fast-growing renewable energy markets in Latin America, as well as the parts of the US and Europe.

The Siemens-Gamesa merger would create a new global market leader in wind energy by capacity, surpassing China’s Goldwind, Denmark’s Vestas and General Electric, according to FTI Consulting.

The merger is broadly considered a win-win in that this move would bring together Siemens’ strength in offshore wind power in mature markets and Gamesa’s leading role in emerging markets.

Each has their own competitive advantage

More specifically, Siemens operates in the mature North American and European markets and whereas Gamesa’s turf are the fast-growing markets such as India, Mexico, and Brazil.

Moreover, Siemens’s wind division, which had almost €6 billion in revenue in 2015, manufactures and installs wind turbines for on- and offshore farms. But the business has been largely focused on the offshore market—where it has a large order backlog for turbines—while fumbling on onshore growth opportunities. Gamesa is also a major player across South America, where it expanded when the Spanish government cut subsidies to clean energy producers in 2013 as well as China and India, where it is the number one foreign producer.

Siemens is known to all of us as a quality engineering company (whose other products include trains, medical body scanners, and technical instruments), but it has struggled to make its wind turbine business profitable. After the merger, it will take a 59 % stake in the company but it will not have a majority on the board but will have five out of the 13 board members in the new group.

Their deal states that in return for Siemens becoming majority shareholder, Siemens will pay Gamesa’s shareholders, which include Spanish utility firm Iberdrola, 1b euros in cash in the form of an extraordinary dividend.

The businesses will be combined within Gamesa which will retain its Madrid headquarters. The Spanish group is creating new shares to be offered to Siemens.

Gamesa has further affirmed that the merged business will be operational by March- April 2017and will be worth 230m euros of earnings before interest and taxes (EBIT) within four years due to the cost and savings strategy that is being implemented. The idea is that getting bigger would also help to lower costs, one of the industry’s key targets in its race for more efficient turbines, which in turn will make it more competitive.