I already wrote about why renewable energy companies are using project finance for their energy infrastructure projects here, be sure to check it out before reading this.

Given the fact that project finance is often an expensive and complicated undertaking, it becomes fundamental to figure whether project finance is a realistic opportunity for a renewable energy project. Keep in mind the following considerations:

Size: Is the project large enough to make PF worthwhile? Banks won’t go through the hassle of PF for small projects, bear in mind that although project finance size varies from country to country, we’re looking at $50m to $100m as being in the ballpark. If the project is too small, both lenders and sponsors will be put off project finance;

Establish Realistic Revenue Streams: Since there are two primary sources of revenue for investors, public funds and the other is revenue streams in the form of charges, paid by end users, sponsors and lenders must figure out what that revenue stream will look like. Will the revenue stream be big enough to support the high debt financing taken by the sponsors?

Length of Project: PF is a long term investment spanning 10-15-20 years so there will be a long payback period;

Physical Assets: Will there be physical assets (solar panels, wind turbine) sufficient to ensure lender repayment in case of default? Banks are going to want more “guarantees”, what is the above-mentioned revenue streams doesn’t come through will they will be able to foreclose on the project’s assets sufficient in value to “make themselves whole,” either by selling the project outright or operating it until the debt is repaid;

Tech Risk: Renewable energy is a very innovative and competitive sector, so tech is evolving quickly. While in many project financings, the tech may be relatively new, generally speaking, project finance lenders do not want to be the first to finance an unproven technology. This is not venture capital. A history of successful use in some context will often be necessary to secure project financing;

Quality of the Contract Network: At the end of the day, project finance is a web of contracts between different parties. It is important to know if the project company has contractual relationships with reputable companies for services key to the success of the project or the technology it employs? Banks will be less keen on lending to a project the success of which depends solely on a few star individuals who may depart, leaving the project unable to meet its potential, so credible contracts are very important;

Receipt of Revenue: In that regard, will the receipt of revenue be enforceable under contractual rights from a creditworthy party? If there is no contract or if the creditworthiness of the purchaser is not credible, this will trigger concern for banks and set off thorough(er) due diligence procedures regarding revenue projections;

Exit Options: What are the ultimate objectives of the sponsors? Are they looking for a quick exit option, do they want to jump ship? Know that once the project is “project financed” and the contracts are in place, divestiture opportunities are complicated by the requirement of the bank consent, and potential purchasers will be thoroughly examined by banks for development and operational expertise as well as creditworthiness;

Risking the Project: In other words, once project financing is completed, the Sponsor will lose the ability to determine how the vast majority of the project’s revenue is spent. In the event a project becomes uneconomic and unable to service its debt, the only option besides refinancing the debt may be to turn over the project to the lenders (voluntarily or involuntarily), with the loss of the Sponsor’s investment in the project.

One of President Trump’s most resounding battle cries during the election was the bold promise to invest in infrastructure. I am going to argue that Mr. Trump should focus on upgrading the US electric grid, most of which is +25 years old and some parts are even +40 years old.

100 years ago, when the original electric grid was built, it was not conceivable to imagine consumers choosing their distributed generation because an energy generator would burn a fossil fuel and create electricity, which would be transmitted to consumer’s homes and that was that.

But the advent of renewable energy and small, private wind and solar producers means that today’s grid is nearing the end of its useful life both physically and functionally. Today the world is much more mobile, fluid, and flexible, but the grid has not kept up. A smart grid is set to provide real benefits to all stakeholders, including consumers, utilities, and regulators.

For starters, it will bring environmental benefits: through efficient use of energy and existing capacity by using digital communications technology to detect and react to local changes in usage and it will give customers options and choices to change their behavior when it comes to the price and type of power they use, and when to use that energy resource efficiently.

Efficiency is optimized thanks to a smart grid because of a two-way power flow and the integration of energy storage capacity, which would allow consumers to take energy when they need it, and the feed it back (in the case of solar/ wind producers) into the grid when prices are higher or store it. However, today, the grid is not really equipped to handle neither reverse power flows nor storage.

The Grid: An Economy Enhancing Investment

Although Americans bemoan the disrepair of their dilapidated roads, transit, and airports in countless NYT editorial pieces, the Trump Administration must consider the unseen but increasingly crucial issue of reinventing the power grid.

While the electric utility sector may not be the most riveting, the U.S. smart grid expenditures forecasts at more than $3 billion in 2017 (PDF) and the global smart grid market expected to surpass $400 billion worldwide by 2020. Navigant Research, a clean tech consultancy, reports on worldwide revenues for smart grid IT (information technology) software and services, are expected to grow from $12.8 billion in 2017 to more than $21.4 billion in 2026.

The private sector is stepping up. Not only tech companies such as Oracle, IBM, SAS, Teradata, EMC, and SAP but also utility giants such as General Electric, Siemens, ABB, Schneider Electric, and Toshiba are getting involved in smart grid IT.

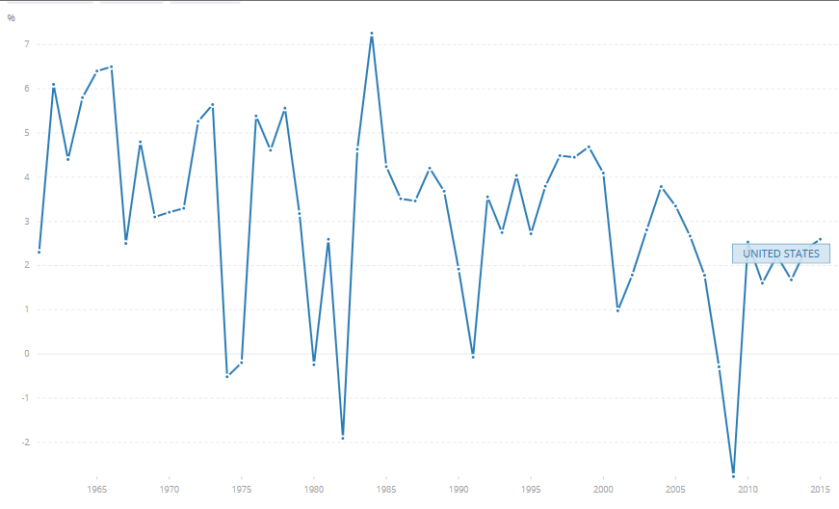

Moreover, with historically low-interest rates (for now) and the potential for infrastructure projects to deliver long-run economic returns, many believe infrastructure investment could kick-start the country’s slowish GDP growth. Yet in spite of a body of economic evidence which points to clear benefits derived from infrastructure investment, simply building more roads will not guarantee economic growth on its own, as the textbook examples: Japan and China indicate. This lesson is particularly important considering the falling returns from public investment in U.S. highways.

U.S GDP Growth % 1965-2015

World Bank Data, 2017

And this brings us to the grid: aiming investment at the grid would improve conditions for millions of people as well as address the needs of the private sector.

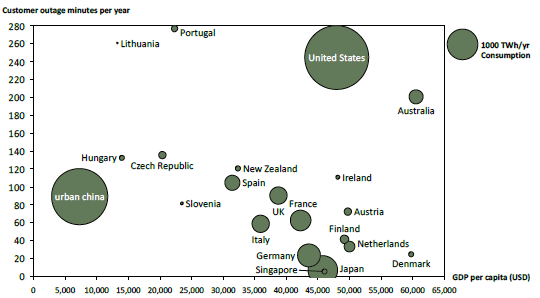

The average American endures 6+ hours of blackouts a year, which amounts to at least $150 billion for the public and private sector each year — about $500 for every man, woman, and child, – that is remarkably bad for a developed country. Power outages in the USA are mostly caused by the effect harsh weather on the aging grid. Heavy industry tends to be most affected by tiny outages, and this example from Saviva Research is painfully illustrative:

A robotic manufacturing facility owned by Toshiba experienced a 0.4-second outage, causing each robot to become asynchronous with the grid; thus short circuiting chips and circuits. Toshiba spent the next 3 months reprogramming each robot, leading to an estimated economic loss of $500m.

International Grid Reliability

Source: Saviva Research 2013

In the U.S, investments in the power grid lag behind Europe. Across the pond, since 2000, the U.K., Italy, Spain, France and Germany have spent a combined $150.3 billion on energy-efficiency programs, compared with $96.7 billion for the U.S, according to data by Bloomberg New Energy Finance. Moreover, according to a 2015 report by energy consultancy, the Rocky Mountain Institute the, the U.S. needs about $2 trillion in grid upgrades by 2030.

The Smart Grid: A Strategic Economy-Enhancing Objective

Yet there is much that the government and the private sector should seek to unpack about consumer behavior, strategic implications, governance, and decision-making regarding the grid, before committing to such a massive investment. The incoming investments in the next decades offer a historically important opportunity to rethink how the whole system of power generation, transmission, and usage operates.

Here’s just one consideration: ownership. Future smart grids are likely to have multiple ownerships, which will most likely span across:

The government: through publicly owned power and transmission lines;

The private sector: independent wind farms developers and operators or utility-owned generators;

Private citizens: owners of household-level battery backup systems or rooftop solar panels.

All it really means is that combining forces for a specific project makes it possible to focus each parties’ inherent assets in the way that best reduces their shared risks, and reduced risk means a lower cost of borrowing, and therefore: cheaper projects.

As J. Michael Barrett explains: If the federal or state government can reduce the investment risk of the project by providing seed capital, issuing tax-exempt bonds, and/or signing a power purchase agreement to buy energy for a guaranteed period of time, the private sector can then provide investment capital at more favorable rates because total project risk is reduced. When all the parties share the up-front construction costs (and risk), promote open access to usable land, and lock-in the commitment of long-term users.

Finally, the most plausible way forward is to invest in new technologies opposed to retrofitting them later, an educated, unideological clear-eyed strategic effort to make the most of these investments would ensure both improved operations improvements in resilience and adaptability across the board.

tl;dr: A functioning integrated electricity system is a basic public good, imperative to the wealth, safety, and wellbeing of any modern society. In the context of a rapidly evolving energy infrastructure landscape, taking a strategic stance during the development of the smart grid in the USA will determine how much value is captured and who will capture it.

Read more: here The Energy Infrastructure that the US Really Needs

Innovation and tech breakthroughs are key drivers of the renewable energy (RE) and clean tech sectors, and in this regard, venture capital (VC) has a powerful grip on the imagination. Indeed, some of the biggest names in tech, like Amazon, Google and Uber are around today thanks to VCs. This has led many to wonder, where are the big, ubiquitous clean tech start-ups that made it big?

Except it’s not as simple as that, collective imagination romanticizes VC, but it is important to separate the myth from the reality and understand that the RE sector is categorically different from IT and tech, and that VC does not lend itself well to the clean tech.

A bit of backstory first: Boom and Bust cycles

In 2005, VC investment in clean tech was in the hundreds of millions. The following year, it increased to $1.75b, according to the National Venture Capital Association. By 2008, investment had skyrocketed to $4.1b (see figure 1). And the US government followed the trend, eager to continue to develop the meteoric rise of promising innovative technologies through a mix of loans, subsidies, and tax breaks. They directed $44.5b into the sector between 2009 and 2011. In other words, the cleantech sector was in full throttle and VCs thought it was ripe for disruption.

Gaddy, Sivaran & O’Sullivan, MIT Working Paper, 2016

But then, due to a confluence of unfavourable events, including:

Fluctuating silicon prices: According to a GTM Research report, high purity silicon (polysilicon), the principal material for solar panels played only a minor role in this price collapse, as over 80% of polysilicon is sold via long-term contracts, and the pricing on these contracts moved little for most of 2011. However, the oversupply in the polysilicon market shifted the spot price of silicon down from $80 per kilogram in late March 2011 to under $30 per kilogram in December, which resulted in a 60% price drop. This lower spot price gave silicon customers the leverage to renegotiate contract pricing downward, and this resulted in much lower realized silicon average selling prices (ASPs) moving forward;

Newly cheapened natural gas (shale boom): Since gas has got so cheap, there was no longer a financial incentive to go with renewables. Technical breakthroughs in natural gas extraction from shale, namely fracking—have opened up reserves so massive that the US has surpassed Russia as the world’s largest natural gas supplier. Because 24% of electricity comes from power plants that run on natural gas, that has kept downward pressure on cost to just 10 cents per kilowatt-hour, and producing significantly less than half the CO2 pollution of coal at that. This new environment made investors divert capital from RE into natural gas;

The 2008 financial crisis: A large proportion of the gains VC firms had made between 2003 and 2007 disappeared, and the sudden and unexpected lack of capital, coupled with the difficulty of taking smaller companies public, hit renewable startups particularly badly. Venture investments in clean tech fell from $4.1 billion in 2008 to $2.5 billion in 2009, which made it difficult to raise money to achieve manufacturing scale;

China’s high paced production of solar infrastructure: Globally increasing demand for solar infrastructure combined with a domestic push on solar manufacturing had propelled China to the top position in terms of PV manufacturing countries. Indeed, since 2004, China’s meteoric production on all fronts of the solar manufacturing value chain, beginning with polysilicon feedstock, to wafers, to cells and modules. By 2008, the ascent of solar industry became so formidable that Chinese firms started reaping economies of scale in the production of purified silicon. By then, China had become the largest PV manufacturer in the world, with 98% of its product shipped overseas.

The clean-tech bubble had burst and the euphoric VC investments came to a swift close. Moreover, shares of public clean tech firms traded at steep discounts to the market peak in 2008, and almost all of the 150 renewable energy start-ups founded in Silicon Valley over the past decade had shut down or were on their last legs. The fallout sent ripples through to every niche in the clean-tech sector: wind, biofuels, electric vehicles, fuel cells and especially solar.

The most prominent casualty of this financial carnage was Solyndra, a start-up designing and manufacturing cylindrical solar tubes, which had received $500 million in federal loan guarantees but after the price of polysilicon crashed they were forced to file for bankruptcy.

The Venture Capital Model: How it works

In a nutshell, VC funds are usually structured as 10-year “partnerships”, where external investors (the limited partners, or LPs) provide capital to the VC fund (run by the experienced general partners, or GPs) to make investments on their behalf. The Model is summed up nicely below.

Zider, Harvard Business Review, 1998

VC investment usually goes like this:

Part 1: A fund will tend to invest in a portfolio of 10-20 start-ups over the first 5 years and harvest the returns in the remaining 5 years.

Part 2: Ideally, sizable returns begin to materialize when a portfolio company is acquired by another firm or when it issues shares on a public market through an initial public offering (IPO)—these events are known as “exits.”

VC funds also tend to invest at several stages of a company’s development, starting with early “seed” rounds, typically $1 million or less, continuing through the next rounds (known as “A”, “B”, “C” rounds). The objective of the VC is to exit and get your returns, but if a company cannot exit within three to five years of raising a major funding round, the VC is likely to write off the investment.

Bear in mind that VCs have contractual investment structures that limit their scope. Take a company that doubles its revenues every year for 20 years, and expands from thousands in revenue to billions, a VC would most likely not touch it, because a VC could not wait 20 years because their funds are could be structured with a requirement to earn returns every 10 years. VC are extremely impatient.

The point of VC is, in theory, to invest in the balance sheet and infrastructure of a company until it reaches sufficient size and credibility so that it can be acquired by a competitor or so that the institutional public-equity markets can step in and provide liquidity. The venture capitalist is, essentially, buyinga cut of someone’s idea, nurturing it for a short period of time so that it becomes profitable, the with the help of an investment bank, exiting.As long as venture capitalists can exit the company, before the company’s’ value ceases rising, they can reap huge returns at a relatively low risk. Indeed, really good VCs operate in “secure” niche environments, where they know the industry inside out, and where traditional low-cost financing is unavailable.

What is a VC’s target investment?

Now, I know, you can point to Tesla, or Boston-Power Inc, a lithium ion battery provider or Sunnova Energy Corp, a provider of residential solar systems, that both raised $250m from VCs, and I agree, there are also many success stories.

In 2014, according to the National Venture Capital Association, the sector as a whole raked in $2b, which is a 41% increase relative to 2013, but it is a 30% decrease compare to 2012. The absolute number of clean tech deals is also up, suggesting that VC are being much more judicious with their investments.

Classically, sectors such as IT and software are ideal recipients of VC. According to Ghosh and Nanda from Harvard, (for more info, check out Ghosh & Nanda, Venture Capital Investment in the Clean Energy Sector. Harvard Business School Working Paper. doi:10.2139/ssrn.1669445), this is mainly due to:

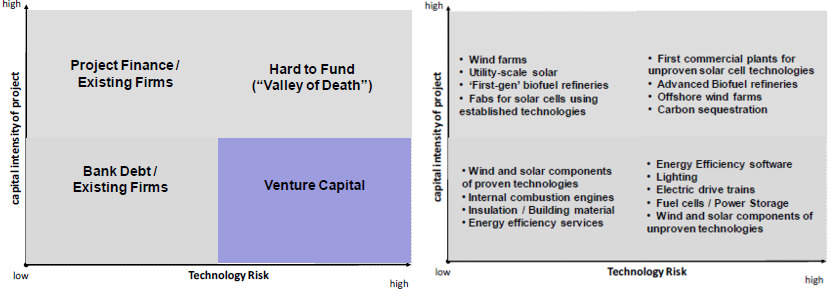

1. Lower levels of capital intensity are highly desirable for VC investors. As you can see in the figure below, the “sweet spot” for VC is typified by high technology risk, but low capital intensity, where a syndicate (a group) of two or three banks can completely fund a start-up through to its IPO.The ability to reduce risk capital and quickly access infrastructure capital is a key differentiator between the IT sector andRE start-up. RE technologies are usually large-scale systems with sizeable physical footprints. They are costly to not only to build but also to operate and maintain. Making a company on the supply side of the energy business requires a serious investment on the industrial side that the VC firms didn’t fully reckon with.

Ghosh & Nanda, Harvard, 2010

2. IT companies have appropriately shorter sales cycles meaning that their products are commercialized promptly, ultimately meaning that VC can exit faster. The textbook example here is Google, that had an IPO 5 years after it received its first round of VC funding and having raised roughly $40m (!) in VC. As many VCs found out the hard way, energy companies don’t operate on those timelines. Consider this analysis by Matthew Nordan, a venture capitalist who specializes in energy and environmental tech. Of all the energy startups that received their first VC funds between 1995 and 2007, only 1.8% gained what he calls the end goal of a VC, meaning an initial public offering on a major exchange.

3. Whilst IT companies face incumbents with high-cost structures, clean energy companies face incumbents like ENI, Shell, and Exxon, who actually have lower cost structures owingto the fact they are giant, well-financed, often more than a century old and established, propped up by diversified investments. And, yes, of course, the average IT company requires infrastructure investment, but it is on a whole other level relative to RE infrastructure, which requires an entire host of investments ranging from diffusors, chillers, arrays and transmission lines,all of which must be manufactured, shipped and installed. It boils down to the fact that an RE company cannot scale and grow as quickly as an IT comply, delaying a potential exit for the VC.

None of this is to say that VC does not have value for RE, it does! VC are often the only private money willing to take the risk of investing in cutting-edge companies, but that’s their niche. Remember that the venture capital niche exists because of the structure and environment of capital markets. Someone with an idea or a new technology often has no other source of financing to turn to. Banks will only finance a new company to the extent to which are hard assets against which to secure the debt, and renewable energy companies and clean tech actually do have hard assets.

tl:dr Renewable energy companies have capital requirements, growth profiles and competitive environments that do not make them ideal candidates for VCs.

Old critiques, die hard. For the longest time, renewable energy (RE) has been viewed as too expensive and un-scalable, as a luxury energy source, that will not be deployed in developing countries. As a matter of fact, how many times did you hear the criticism, that by diverting investment away from so-called “cheap” fossil fuel energy, we would be depriving developing countries of their right to develop?

The numbers quantifying investments in RE are in! It should be no surprise that RE investment is increasing significantly and the developing world, especially China, is leading the way.

The findings of the United Nations Environment Programme (UNEP) Global Trends in Renewable Energy Investments 2016 confirmed that RE set new records in 2015 for dollar investments, the amount of new capacity added and the relative importance of developing countries in the context of that growth.

Record-breaking uptrend in Renewable Energy Investments

Global investment in RE rose 5% to $285.9 billion from 2014 to 2015, breaking the previous record of $278.5 billion reached in 2011 (FYI that’s double the dollar allocations to new coal and gas generation, which was an estimated $130 billion in 2015) when the famous ‘green stimulus’ programs in German and Italian were in full throttle. The figure below shows that the 2015 investment increased sixfold since 2004 and that investment in RE has not been below $230b since 2010.

GLOBAL NEW INVESTMENT IN RE BY ASSET CLASS, 2004-2015, $BN

Source: UNEP, Bloomberg New Energy Finance

*Asset finance volume adjusts for re-invested equity. Total values include estimates for undisclosed deals.

Over the course of the 12 years shown in the chart, the cumulative RE investment has reached $2.3 trillion.

Moreover, in 2015 some 134GW of RE excluding large hydro were commissioned, equivalent to some 53.6% of all power generation capacity completed in that year – and this is worth mentioning because it is the first time it has represented a majority. Of the renewables total, wind accounted for 62GW installed, and solar photovoltaics 56GW, highest ever figure and sharply up from their 2014 additions of 49GW and 45GW respectively.

Developing Countries Leading the Way

The investment which led to record-breaking levels came from China, which lifted its investment by 17% to $102.9 billion, about 36% of the global total. In the Middle East and Africa, investment was up a total of 58% at $12.5 billion, helped by project development in especially in South Africa and Morocco; and in India, up 22% at $10.2 billion.

More significantly, 2015 was the first year in which investment in RE (excluding large hydro) was higher in developing economies than in developed countries. The figure below shows that the developing world invested $156 billion last year, some 19% up on 2014 and a remarkable 17 times the equivalent figure for 2004, of $9 billion.

INVESTMENT IN RE: DEVELOPED/ DEVELOPING COUNTRIES, 2004-2015, $BN

source: UNEP, Bloomberg

The key contributors to this shift from developed to developing are the big three: China, India, and Brazil, who saw an investment rise of 16% to $120.2 billion

A large part of the record-breaking investment in developing countries took place in China. Indeed China has been the single biggest reason for the strong increasing trend for the developing world as a whole since 2004. In spite of low market fundamentals and much talk of decreased investment in RE, China has been a key contributor to these figures. China invested $102.9 billion in 2015, up 17%, representing well over a third of the global total.

Likewise, India enjoyed a second successive year of increasing investment, breaching the $10 billion for the first time since 2011.

Other developing countries, excluding the big three, lifted their investment by 30% last year to an all-time high of $36 billion, some 12x their 2004 investment, the biggest players are:

South Africa also deserves an honorable mention as it’s RE investment is up 329% at $4.5 billion significantly ramping up their solar PV, in the context of their auction program. In June last year, the government in Pretoria launched a tender for an additional 1.8GW for its renewables program. One of the signal deals later in the year was the financing in September of the 100MW Redstone solar thermal project for an estimated $756m, helped by loans from the World Bank’s International Finance Corporation and Overseas Private Investment Corporation of the US;

Mexico saw a 105% increase at $4 billion, aided by investment from the development bank Nafin for 9 wind projects. Moreover, Mexico is emerging as an important location for bond issues to back renewable energy projects. In November last year, National Financiera issued $500 million worth of five-year bonds to contribute towards the development of nine wind farms with a total capacity of 1.6GW;

Chile saw an increase of 151% higher at $3.4 billion, thanks to a sizable uptrend in solar project financings;

Morocco, Turkey, and Uruguay also saw investment increases in excess of the $1 billion milestone in 2015.

Developed world downward trend (mostly)

In the developed world, however, we are witnessing a downward trend quite consistently, since 2011, when it peaked at $191 billion, some 47% higher than the 2015 outturn. Developed countries invested $130 billion in 2015, down 8% and their lowest figure since 2009. This decline is due to two major factors:

because of the US, where firstly; there was a rush of investment in 2011 as projects and companies tried to catch the Treasury grant and Federal Loan Guarantee programmes before they expired and secondly, the US Supreme Court’s decision in February 2016 to allow all legal objections to the Environmental Protection Agency’s Clean Power Plan to be heard before it can be implemented may be deterring investment in 2016.

but much more to do with Europe, where allocations fell by 60% between 2011 and 2015. That big drop was caused by a mix of factors including retroactive cuts in support for existing projects in Spain, Romania and several other countries, an economic downturn in southern Europe that made electricity bills more of a political hot potato, the cut of government subsidies aimed at incentivizing RE in Germany and Italy, and the big fall in the cost of PV panels over recent years.Italy, in particular, saw renewable energy investment of just under $1 billion, down 21% on 2014 and far below the peak of $31.7 billion seen during the PV boom of 2011.

Retroactive cuts to feed-in tariffs really weaken support for solar energy investments. Spain, scene of particularly painful retroactive revenue cuts imposed by the government during the 2011-14 period, and the end of all support for new projects, saw investments of just $573 million in 2014. This was slightly up on the previous year but miles below the $23.6 billion peak of 2008.

But it’s not all bad in Europe, especially since the UK has not seen a significant slowdown in RE investments in recent years, and is actually pushing in the opposite direction. Moreover, in spite of the fact that offshore wind in the North Sea has seen massive investments amounting to $17b, Europe’s aggregate RE investment is still in decline.