Innovation and tech breakthroughs are key drivers of the renewable energy (RE) and clean tech sectors, and in this regard, venture capital (VC) has a powerful grip on the imagination. Indeed, some of the biggest names in tech, like Amazon, Google and Uber are around today thanks to VCs. This has led many to wonder, where are the big, ubiquitous clean tech start-ups that made it big?

Except it’s not as simple as that, collective imagination romanticizes VC, but it is important to separate the myth from the reality and understand that the RE sector is categorically different from IT and tech, and that VC does not lend itself well to the clean tech.

A bit of backstory first: Boom and Bust cycles

In 2005, VC investment in clean tech was in the hundreds of millions. The following year, it increased to $1.75b, according to the National Venture Capital Association. By 2008, investment had skyrocketed to $4.1b (see figure 1). And the US government followed the trend, eager to continue to develop the meteoric rise of promising innovative technologies through a mix of loans, subsidies, and tax breaks. They directed $44.5b into the sector between 2009 and 2011. In other words, the clean tech sector was in full throttle and VCs thought it was ripe for disruption.

But then, due to a confluence of unfavourable events, including:

- Fluctuating silicon prices: According to a GTM Research report, high purity silicon (polysilicon), the principal material for solar panels played only a minor role in this price collapse, as over 80% of polysilicon is sold via long-term contracts, and the pricing on these contracts moved little for most of 2011. However, the oversupply in the polysilicon market shifted the spot price of silicon down from $80 per kilogram in late March 2011 to under $30 per kilogram in December, which resulted in a 60% price drop. This lower spot price gave silicon customers the leverage to renegotiate contract pricing downward, and this resulted in much lower realized silicon average selling prices (ASPs) moving forward;

- Newly cheapened natural gas (shale boom): Since gas has got so cheap, there was no longer a financial incentive to go with renewables. Technical breakthroughs in natural gas extraction from shale, namely fracking—have opened up reserves so massive that the US has surpassed Russia as the world’s largest natural gas supplier. Because 24% of electricity comes from power plants that run on natural gas, that has kept downward pressure on cost to just 10 cents per kilowatt-hour, and producing significantly less than half the CO2 pollution of coal at that. This new environment made investors divert capital from RE into natural gas;

- The 2008 financial crisis: A large proportion of the gains VC firms had made between 2003 and 2007 disappeared, and the sudden and unexpected lack of capital, coupled with the difficulty of taking smaller companies public, hit renewable startups particularly badly. Venture investments in clean tech fell from $4.1 billion in 2008 to $2.5 billion in 2009, which made it difficult to raise money to achieve manufacturing scale;

- China’s high paced production of solar infrastructure: Globally increasing demand for solar infrastructure combined with a domestic push on solar manufacturing had propelled China to the top position in terms of PV manufacturing countries. Indeed, since 2004, China’s meteoric production on all fronts of the solar manufacturing value chain, beginning with polysilicon feedstock, to wafers, to cells and modules. By 2008, the ascent of solar industry became so formidable that Chinese firms started reaping economies of scale in the production of purified silicon. By then, China had become the largest PV manufacturer in the world, with 98% of its product shipped overseas.

The clean-tech bubble had burst and the euphoric VC investments came to a swift close. Moreover, shares of public clean tech firms traded at steep discounts to the market peak in 2008, and almost all of the 150 renewable energy start-ups founded in Silicon Valley over the past decade had shut down or were on their last legs. The fallout sent ripples through to every niche in the clean-tech sector: wind, biofuels, electric vehicles, fuel cells and especially solar.

The most prominent casualty of this financial carnage was Solyndra, a start-up designing and manufacturing cylindrical solar tubes, which had received $500 million in federal loan guarantees but after the price of polysilicon crashed they were forced to file for bankruptcy.

The Venture Capital Model: How it works

In a nutshell, VC funds are usually structured as 10-year “partnerships”, where external investors (the limited partners, or LPs) provide capital to the VC fund (run by the experienced general partners, or GPs) to make investments on their behalf. The Model is summed up nicely below.

VC investment usually goes like this:

- Part 1: A fund will tend to invest in a portfolio of 10-20 start-ups over the first 5 years and harvest the returns in the remaining 5 years.

- Part 2: Ideally, sizable returns begin to materialize when a portfolio company is acquired by another firm or when it issues shares on a public market through an initial public offering (IPO)—these events are known as “exits.”

VC funds also tend to invest at several stages of a company’s development, starting with early “seed” rounds, typically $1 million or less, continuing through the next rounds (known as “A”, “B”, “C” rounds). The objective of the VC is to exit and get your returns, but if a company cannot exit within three to five years of raising a major funding round, the VC is likely to write off the investment.

Bear in mind that VCs have contractual investment structures that limit their scope. Take a company that doubles its revenues every year for 20 years, and expands from thousands in revenue to billions, a VC would most likely not touch it, because a VC could not wait 20 years because their funds are could be structured with a requirement to earn returns every 10 years. VC are extremely impatient.

The point of VC is, in theory, to invest in the balance sheet and infrastructure of a company until it reaches sufficient size and credibility so that it can be acquired by a competitor or so that the institutional public-equity markets can step in and provide liquidity. The venture capitalist is, essentially, buying a cut of someone’s idea, nurturing it for a short period of time so that it becomes profitable, the with the help of an investment bank, exiting. As long as venture capitalists can exit the company, before the company’s’ value ceases rising, they can reap huge returns at a relatively low risk. Indeed, really good VCs operate in “secure” niche environments, where they know the industry inside out, and where traditional low-cost financing is unavailable.

What is a VC’s target investment?

Now, I know, you can point to Tesla, or Boston-Power Inc, a lithium ion battery provider or Sunnova Energy Corp, a provider of residential solar systems, that both raised $250m from VCs, and I agree, there are also many success stories.

In 2014, according to the National Venture Capital Association, the sector as a whole raked in $2b, which is a 41% increase relative to 2013, but it is a 30% decrease compare to 2012. The absolute number of clean tech deals is also up, suggesting that VC are being much more judicious with their investments.

Classically, sectors such as IT and software are ideal recipients of VC. According to Ghosh and Nanda from Harvard, (for more info, check out Ghosh & Nanda, Venture Capital Investment in the Clean Energy Sector. Harvard Business School Working Paper. doi:10.2139/ssrn.1669445), this is mainly due to:

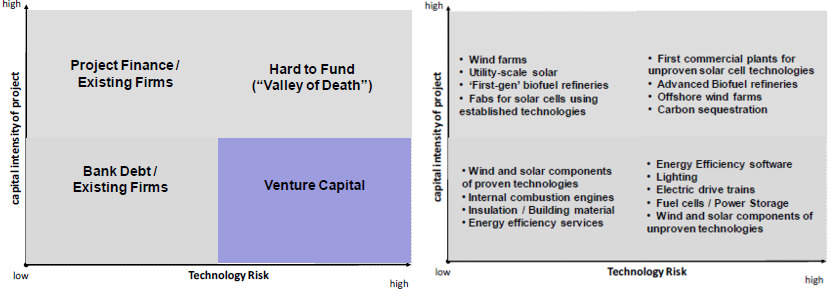

1. Lower levels of capital intensity are highly desirable for VC investors. As you can see in the figure below, the “sweet spot” for VC is typified by high technology risk, but low capital intensity, where a syndicate (a group) of two or three banks can completely fund a start-up through to its IPO. The ability to reduce risk capital and quickly access infrastructure capital is a key differentiator between the IT sector and RE start-up. RE technologies are usually large-scale systems with sizeable physical footprints. They are costly to not only to build but also to operate and maintain. Making a company on the supply side of the energy business requires a serious investment on the industrial side that the VC firms didn’t fully reckon with.

2. IT companies have appropriately shorter sales cycles meaning that their products are commercialized promptly, ultimately meaning that VC can exit faster. The textbook example here is Google, that had an IPO 5 years after it received its first round of VC funding and having raised roughly $40m (!) in VC. As many VCs found out the hard way, energy companies don’t operate on those timelines. Consider this analysis by Matthew Nordan, a venture capitalist who specializes in energy and environmental tech. Of all the energy startups that received their first VC funds between 1995 and 2007, only 1.8% gained what he calls the end goal of a VC, meaning an initial public offering on a major exchange.

3. Whilst IT companies face incumbents with high-cost structures, clean energy companies face incumbents like ENI, Shell, and Exxon, who actually have lower cost structures owing to the fact they are giant, well-financed, often more than a century old and established, propped up by diversified investments. And, yes, of course, the average IT company requires infrastructure investment, but it is on a whole other level relative to RE infrastructure, which requires an entire host of investments ranging from diffusors, chillers, arrays and transmission lines, all of which must be manufactured, shipped and installed. It boils down to the fact that an RE company cannot scale and grow as quickly as an IT comply, delaying a potential exit for the VC.

None of this is to say that VC does not have value for RE, it does! VC are often the only private money willing to take the risk of investing in cutting-edge companies, but that’s their niche. Remember that the venture capital niche exists because of the structure and environment of capital markets. Someone with an idea or a new technology often has no other source of financing to turn to. Banks will only finance a new company to the extent to which are hard assets against which to secure the debt, and renewable energy companies and clean tech actually do have hard assets.

tl:dr Renewable energy companies have capital requirements, growth profiles and competitive environments that do not make them ideal candidates for VCs.

Cover photo by Max Mudie/Alamy

Interesting article, i agree that the energy industry is not the ideal candidate for a venture capital

LikeLike