Bloomberg New Energy Finance reports that Danish wind manufacturer Vestas reclaimed the top spot in the annual ranking of wind turbine manufacturers.

Top Onshore Turbine Manufacturers, 2016

BNEF 2017

🇩🇰 Vestas has been on the scene since 1945 as an appliance manufacturer and moved into turbine production in 1979 and has plants in Denmark, Germany, India, Italy, Romania, the United Kingdom, Spain, Sweden, Norway, Australia, China, and the United States. They installed a whopping 8.7GW of turbines in 2016, good for 16% of all onshore wind installations last year. 43% of those 8.7GW were in the USA. Vestas has a very international reach and is continuing to pursue a global strategy with projects commissioned in 35 countries, more than any other turbine maker.

🇺🇸 General Electric placed second with 6.5GW, some 0.6GW more than in 2015. They are the largest producer in the USA and while they narrowly lost its traditional lead in the US market for newly commissioned turbines to Vestas, GE managed to increase its global presence to 21 countries in 2016, from 14 in 2015.

🇨🇳 Xinjiang Goldwind Science & Technology fell from first to third place with 6.4GW in 2016. Virtually all of the Chinese manufacturer’s capacity was built in its home market, where Goldwind further extended its market share. China’s contracting wind market had a clear impact on Goldwind, as overall installations were 22.8GW, down 21% from the record 29GW in 2015.

🇪🇸 Gamesa came in fourth and reported that it had beaten its own annual turbine manufacturing record, having already made more than 1,880 units with a total productive capacity of 3,880 MW. The new record was a long time in the making, taking eight years to beat 2008’s 3,787 MW. Their record was set with turbines assembled all over the world — India (36%), Europe (28%), China (26%) and Brazil (10%). Almost one in three Gamesa turbines was installed in India.

🇩🇪 Enercon sits in 5th place, with a market share of 7.2% worldwide and 59.2% only in Germany. Enercon has production facilities in Germany, Sweden, Brazil, India, Canada, Turkey, and Portugal. They are limited to onshore wind turbines.

🇩🇪 Nordex, in 6th place has installed wind power capacity of more than 18 GW in over 25 markets. The production network comprises plants in Germany, Spain, Brazil, the United States and soon also India. Nordex closed the first half of 2016 with a new record in German installations, with a total 134 new turbines installed marks an increase of 135% over the same period in the previous year

🇨🇳 Guodian / United Power is the Chinese runner-up, with its manufacturing spread entirely across China. Originally, a joint venture with Westinghouse and later a joint venture with Siemens from 1998 to 2006 before restructuring to a state-owned enterprise in 2007. Today, they have 23,030 MW of wind power installed, they have grown rapidly and strategically in the last 15 years.

🇩🇪 Siemens Wind Power in 8th place seems to be coming in short, but this is because this list looks at onshore wind, whilst Siemens supplies about 60% of European offshore wind turbines.

🇨🇳 Ming Yang 明阳风电 is the largest privately owned wind turbine manufacturer in China.

🇨🇳 Envision, the “smallest” Chinese entrant, Since its foundation in 2007, Envision Energy has maintained rapid growth in its business operations.

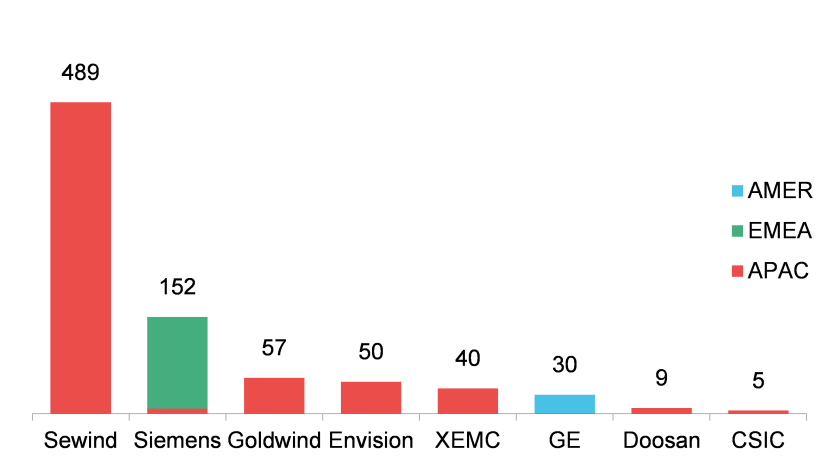

Top Offshore Turbine Manufacturers, 2016

BNEF, 2017

🇨🇳 Sewind is the undisputed offshore leader, supplying nearly 60% of the 832 MW of new offshore wind turbines commissioned in 2016 globally and since it manufactures Siemens offshore turbines under license in China, the company actually installed 388 MW of Siemens turbines and 101 MW of own design machines.

What to expect next

I wrote about the upcoming merger between Gamsea and Siemens a few months ago here and the merger between the two is set to go through. It appears that they are aiming at speeding up consolidation due to competition and price pressures. As Gamsea and Siemens combine their wind-turbine manufacturing businesses, creating a company that will dominate the industry, Vestas will be dethroned to second place.

A recent report by the Global Wind Energy Council (GWEC) shows that China installed 592 MW of offshore wind in 2016, entering the global top three alongside Germany and the Netherlands. Although the GWEC and BNEF reports focus on different aspects, both point to a steady rise in Asian offshore wind markets. This is also evident in day to day new reports on deals and contracts.

There are some interesting developments in terms of who’s got skin in the equity game in renewable energy. What’s really interesting to me is that the equity investment landscape has transformed quite a bit in the last few years and in this post we’ll see how and why.

But first, remember that, according to the OECD, there are three (main) ways to finance renewable energy projects:

Project Finance: This involves a mixture of debt (usually from banks) and equity capital (we will go into more detail below). According to Bloomberg, 2015 was the first year in which project finance constitutes more than half of total asset finance in RE electricity. Remember that project finance involves creating a Special Purpose Vehicle (SPV) with its cash flows separated from those of its sponsor companies;

On-the-balance sheet financing: Done by utilities (EDF, ENEL, Suez), independent power producers and other project developers. On the balance sheet financing, makes up over 47% of total asset finance in RE, about 94 billion;

Project Bonds: Project Bonds, these do not include corporate bonds or government bonds. They account for a small fraction of financing.

Nevertheless, there are other emerging financial structures, which I can go into in another post, but venture capital is one of them. Utilities are substantial providers of equity capital in the renewable sector. However, due to the large scale investment and stable income returns, there is greater interest from the financial services industry.

This brings us to wind equity financing

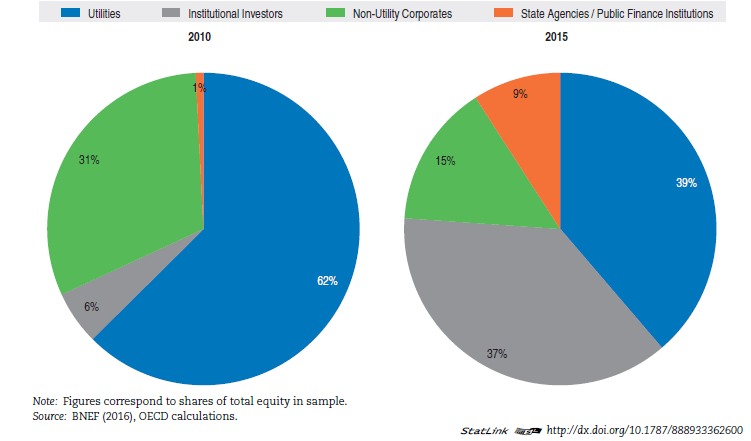

Back in the day, the first offshore wind-power farms were usually financed on the balance sheets of the utilities that planned, built, and operated them. Today, there are many more players involved, such as banks, private equity funds, pension funds, state-backed “green” banks (such as the Green Investment Bank, the Nordic Investment bank and the European Investment Bank) and insurance companies. The graph below shows how the equity mix has morphed in the last couple of years.

Change in Equity Mix for Wind Energy

The share of equity provided by utilities is steadily shrinking as other players get involved, decreasing from 62% in 2010 to 39% in 2015, and that of non-utility corporates from 31% to 15%. In other words, the combined share of the two traditional equity investors in the wind energy sector decreased substantially, from 93% in 2010 to 54% in 2015. Accordingly, other investors have stepped up their game. One of the possible explanations for this decrease may potentially be due to deleveraging as a consequence of the financial crisis.

The Rise of Institutional Investors

For brownfield wind projects, meaning wind projects where there is already existing infrastructure and possibly licenses as well, institutional investors such as pension funds, insurance companies, private equity and infrastructure funds have become major equity investors. According to the OECD, their cut in total equity provisions increased from 6% in 2010 to a staggering 37% in 2015, making them the second most important equity providers in the 2015 sample, just 1% behind utilities. This sharp increase of equity provision by institutional investors can be traced mainly to the acquisition of brownfield assets or portfolios for onshore wind deals. Pension funds and insurers were not involved in any greenfield onshore wind-power transactions included in the OECD 2015 sample.

This trend suggests that institutional investors look to the onshore wind sector mainly for the acquisition of existing projects.Such a strategy presents several advantages:

Lower Costs: Existing projects are already (usually) built, and there they do not need to start from scratch;

“Up to Code”: Lengthy permits, licensing and commissioning agreements may already be in place and therefore do not need to be requested;

Fast Deployment: Ultimately the project can be up and running (and earning) in less time.

Moreover, equity financing in wind energy assets by state agencies and public finance institutions grew from a negligible cut in 2010 to 9% of total equity invested in 2015. This sharp increase can be linked directly to the investments done by the UK Green Investment Bank. The UK’s GIB, an institution created by the UK government in 2012 with the aim of attracting private sector financing for green infrastructure projects. The creation or expansion of similar institutions is a trend observable at the global level and is important for risk sharing with newer technologies. Take offshore wind, for example, as projects scale up and move into deeper water, newer technologies also add to construction risk. This may be a barrier to entry and discourage some investors from participating.

In Europe, commercial banks have started partnering up with government supported banks (United Kingdom’s Green Investment Bank, Germany’s KfW Development Bank), export credit agencies (Denmark’s EKF and Belgium’s Delcredere – Ducroire and Italy’s SACE), and multilateral banks (the European Investment Bank) as a way to provide equity financing to wind projects .

The diversification of participants is good for everyone, because:

Risk: The risk that corresponds to the project is diversified across an array of investors, meaning that investors are more likely to invest if they do it along other reputable investors, rather than going in it solo;

Mainstreaming: the diversification of participants shows that equity financing for RE is no longer as niche as it was, with pension funds and insurance companies putting skin in the game.

Example: The Galloper Offshore Wind Farm

The largest wind equity deal in Europe in 2015 the the Galloper Offshore Wind Farm. It’s a project that will be completed in 2018, located off the coast if Suffolk, east England.

The equity investors are:

Innogy RenewablesUK, a subsidiary of the German utility company RWE

The UK’s Green Investment Bank, a public finance institution

Macquarie Capital, an institutional investor

Siemens Financial Services, a subsidiary of Siemens, a corporation

Sumitomo Corporation, a corporation

This array of private and public investors is an example of what the equity landscape is shifting towards.

So why did the equity investing landscape change?

The explosion of new capacity additions fostered equity market growth for wind projects. New projects not only became more frequent but they also grew in average size, requiring more capital. It would only be normal to have several new, independent developers enter the sector under such favorable market conditions. Moreover, many utilities have been financially constrained due to the difficulties in the merchant power sector, further limiting their contribution to the sector.

The take-home message we can draw from this is that as the demand for wind energy increased so did the associated capital requirements. Utilities and developers did not have the necessary capital to cover demand, so third party investors were roped in. Likewise, corporations like Siemens and Sumitomo are using their financial strength to offer financing directly to smaller developers.

Preamble: I would like to point out that I truly prefer not to engage in these types of discussions (read: I’m over it), because the sources of information that are available to me, are available to everyone else. I also do not consider it my duty to educate every Tom, Dick, and Henry on climate change. However, in light of recent developments, we will probably be encountering a more energized brand of deniers, so here is a non-exhaustive list of answers I took from Robert Henson’s Rough Guide to Climate Change.

Since the days of Roger Revelle, the pioneering oceanographer whose body of work was instrumental for our understanding of the role of greenhouse gas emissions in our atmosphere, deniers developed certain criticisms that are still popular today. I believe that these arguments will keep on cropping up for as long as there is a “debate” on climate change, so it’s best that we equip ourselves with appropriate answers.

Taken to the extreme, anti climate change arguments can be summed up in the following quote:

“The atmosphere isn’t warming; and if it is, then it’s due to natural variation; and even if it’s not due to natural variation, then the amount of warming is insignificant; and if it becomes significant, then the benefits will outweigh the problems; and even if they don’t, technology will come to the rescue;and even if it doesn’t, we shouldn’t wreck the economy to fix the problem when many parts of the science are uncertain.”

Toles 2006, Washington Post

“But the atmosphere isn’t warming….”

According to an ongoing temperature analysis conducted by scientists at NASA’s Goddard Institute for Space Studies (GISS), the average global temperature on Earth has increased by a mean of about 0.8° Celsius (1.4° Fahrenheit) since 1880. Two-thirds of the warming has occurred since 1975, at a rate of roughly 0.15-0.20°C per decade.

This arguement, has seeminly been put to rest, yet deniers seem to resist it, possibly because they do no think that a global mean warming of 0.8°C is a big deal. Here is a more vivd statistical example of what that means:

Dr. Arun Majumdar’s presentation, Michigan State University

This is a bell curve mapping distribution of temperature anomalies over 60 years. To the left are temperatures colder than average and to the right are temperatures hotter than average. The mean is shifting and the distribution is broadening rightwards. The right tail of the distribution is reaching 4 and 5 sigma, which are probabilities that were unheard of decades ago. The anomalies occurring at 4 and 5 sigma are (were) rare massive heatwaves, storms, and floods, which are becoming more common then ever.

“Okay, but I still went skiing this winter…”

The weather and the climate are two different things. The difference between weather and climate is a measure of time. Weather is what conditions of the atmosphere are over a short period of time, and climate is how the atmosphere “behaves” over relatively long periods of time. We talk about climate change in terms of years, decades, and centuries. The weather is forecast 5 0r 10 days ahead, but the climate is studied across long periods of time to look for trends or cycles of variability, such as the changes in wind patterns, ocean surface temperatures, and precipitation. Snow in skiing locations isn’t proof that climate change is not happening.

“The warming is due to natural variation…”

This is a very common argument, the denier does not argue against the existence of climate change, generously admitting the climate has *always* changed, but they do not believe that humans are responsible for it.

The IPCC has concluded that the warming of the last century, especially from the 1970s, falls outside the bounds of natural variability.

Variation of Co2 in atmosphere, from 800000BC to today, NOAA NCDC

Let’s walk down memory lane and look at what the IPCC has been saying to us for 26 years. And keep in mind that the IPCC reports are the most comprehensive, global, and peer-reviewed studies on climate change ever written by anyone, bringing together the work of over 800 scientists, more than 450 lead authors from more than 130 countries, and more than 2,500 expert reviewers. In short, the IPCC reports are humanity’s best attempt to date at getting the science right.

Over the last 800,000 years, Earth’s climate has been cooler than today on average, with a natural cycle between ice ages and warmer interglacial periods. Over the last 10,000 years (since the end of the last ice age) we have lived in a relatively warm period with stable CO2 concentration. Humanity has flourished during this period. Some regional changes have occurred – long-term droughts have taken place in Africa and North America, and the Asian monsoon has changed frequency and intensity – but these have not been part of a consistent global pattern.

The rate of CO2 accumulation due to our emissions in the last 200 years looks very unusual in this context (see chart above). Atmospheric concentrations are now well outside the 800,000-year natural cycle and temperatures would be expected to rise as a result.

Moreover, the IPCC in 1995, in its second assessment report included a sentence that hit the headlines worldwide:

“The balance of evidence suggests a discernible human influence on global climate”

By 2001, IPPC’s third report was even clearer:

“There is an new and stronger evidence that most of the warming observed over the last 50 years is attributable to human activities.”

By 2007, in it’s fourth report, IPCC spoke more strongly still:

“Human induced warming of the climate system is widespread”

In 2013, in the 5th Assessment Report, they stated,

“It is extremely likely that human influence on climate caused more than half of the observed increase in global average surface temperature from 1951 to 2010”

Human activity has led to atmospheric concentrations of carbon dioxide, methane and nitrous oxide that are unprecedented in at least the last 800,000 years.

There is, therefore, a clear distinction to be made between what is “natural variability” and what is our contribution.

“The amount of warming is insignificant…”

The European Geosciences Union published a study in April 2016 that examined the impact of a 1.5°C vs. a 2.0°C (bear in mind we are at 0.8°C now, without the slightest chance of slowing down) temperature increase by the end of the century. It found that the jump from 1.5 – 2°C, a third more of an increase, raises the impact by about that same fraction, on most of the natural phenomena the study covered. Heat waves would last around a third longer, rain storms would be about a third more intense, the increase in sea level would be that much higher and the percentage of tropical coral reefs at risk of severe degradation would be roughly that much greater.

But in other cases, that extra increase in temperature makes things ever more dire. At 1.5°C, the study found that tropical coral reefs stand a chance of adapting and reversing a portion of their die-off in the last half of the century. But at 2°C, the chance of recovery disappears. Tropical corals are virtually wiped out by the turn of the century.

With a 1.5°C rise in temperature, the Mediterranean area is forecast to have about 9% less fresh water available. At 2°C, that water deficit nearly doubles. So does the decrease in wheat and maize harvest in the tropics.

Bottom line: It may look small but it’s a huge deal.

“The benefits will outweigh the problems”

When people talk of alleged benefits of climate change, they are usually talking about agriculture. The argument says that the increased concentrations of CO2 will give a boost to crop harvests leading to larger yields.

This is laughable

Climate change will slow the global yield growth because high temperatures result in shorter growing seasons. Shifting rainfall patterns can also reduce crop yields. Climate trends are already believed to be diminishing global yields of maize and wheat. These symptoms will only worsen as temperatures and extreme weather events become more common. If climate change is allowed to reach a point where the biophysical threshold is exceeded, as would be the case on current emission trajectories, then crop failure will become normal. Also, the severest risks are faced by countries with high existing poverty and dependence on agriculture for livelihoods. Even at “low” levels of warming, vulnerable areas will suffer serious impacts.

Sub-Saharan Africa, according to the World Economic Forum, at 1.5°C warming by 2030 would bring about a 40% loss in maize cropping areas;

South East Asia, in a 2°C would experience unprecedented heat extremes in 60%-70% of their areas.

Agricultural productivity is at risk, not only in developing countries but also in breadbasket regions such as North and South America, the Black Sea and Australia.

Moreover, in October 2015, a study published in Nature estimated that the world could see a 23% drop in global economic output by 2100 due to a changing climate, compared to a world in which climate change is not taking place. The coauthor of the study had this to say,

“Historically, people have considered a 20% decline in global GDP to be a black swan: a low-probability catastrophe – Instead, we’re finding it’s more like the middle-of-the-road forecast.”

“Technology will come to the rescue…”

Deniers who make this case seemingly acknowledge climate change, yet they are optimistic believers in technology being the be-all end-all and that geo-engineering will save us from the clutches of global warming. There are two things I find problematic about this approach:

I think this argument is akin to the “We almost discovered nuclear fusion- we’re only 20 years away!” argument, which stipulates that the nuclear fusion is at any given point in time 20 years away. It takes into account that we have not developed the appropriate technologies to “save” us from climate change, and when we do, there is still a maddening lag between the innovation and deployment. Not to mention the fact we still have not identified which technologies can do the greatest good in the shortest time so we cannot fly blindly in a vague hope that tech will rescue us;

Such an approach fights the “symptoms” of climate change, not the cause of it, meaning that it entrenches our extremely wasteful and inefficient ways that have brought on climate change in the first place.

None of this is to say that I do not believe that technology will play a pivotal role in our transition, of course, it will! But we cannot afford to rely entirely on waiting for carbon capture and storage and the likes to become a deployable and scalable economic reality.

“We shouldn’t wreck the economy to fix the problem when it’s still uncertain!”

When you really get down do it, people will just tell you what their ultimate bottom-line is. If we don’t know with absolute confidence how much you warmer and what the local and regional impact will be perhaps we’d better not committing ourselves to costly reductions in greenhouse gas emissions.

I have written a post on the employment benefits tied to jobs in the renewable energy sector, and there are a plethora of studies pointing to the huge costs of climate change inaction, amongst these, a new study by scholars from the LSE, published last year in Nature Climate Change, offers a daunting scenario.

They estimate that a business-as-usual emissions path would lead to expected warming of 2.5 degrees C by 2100. Under that scenario, banks, pension funds, and investors could sacrifice up to $2.5 trillion in value of stocks, bonds, and other financial assets. The worst-case scenario, with a 1% chance of occurring, would put $24 trillion (about 17 % of global financial assets) at risk. This is but one of the scenarios that have been studied, that point to the huge costs of inaction.

Climate change can affect the economy in myriad ways; including the extent to which people can perform their jobs, how productive they are at work, and the effects of shifting temperatures and precipitation patterns on things like agricultural yields or manufacturing processes. These factors help determine our “economic output” — all the goods and services produced by an economy.

In spite of the fact that there is disagreement on how much exactly economies will be affected, we know the cost of inaction will be immense. With the information at our disposal, it would be foolish and dangerous to assume that reducing emissions will cost more than coping with a changing climate.

Good luck with your “debate” and let me know how it goes.