There are some interesting developments in terms of who’s got skin in the equity game in renewable energy. What’s really interesting to me is that the equity investment landscape has transformed quite a bit in the last few years and in this post we’ll see how and why.

Renewable Energy Asset Financing, 2004-2015

But first, remember that, according to the OECD, there are three (main) ways to finance renewable energy projects:

- Project Finance: This involves a mixture of debt (usually from banks) and equity capital (we will go into more detail below). According to Bloomberg, 2015 was the first year in which project finance constitutes more than half of total asset finance in RE electricity. Remember that project finance involves creating a Special Purpose Vehicle (SPV) with its cash flows separated from those of its sponsor companies;

- On-the-balance sheet financing: Done by utilities (EDF, ENEL, Suez), independent power producers and other project developers. On the balance sheet financing, makes up over 47% of total asset finance in RE, about 94 billion;

- Project Bonds: Project Bonds, these do not include corporate bonds or government bonds. They account for a small fraction of financing.

Nevertheless, there are other emerging financial structures, which I can go into in another post, but venture capital is one of them. Utilities are substantial providers of equity capital in the renewable sector. However, due to the large scale investment and stable income returns, there is greater interest from the financial services industry.

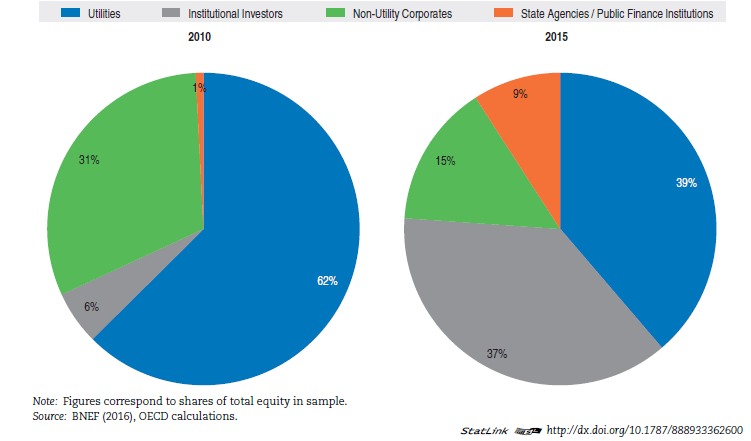

This brings us to wind equity financing

Back in the day, the first offshore wind-power farms were usually financed on the balance sheets of the utilities that planned, built, and operated them. Today, there are many more players involved, such as banks, private equity funds, pension funds, state-backed “green” banks (such as the Green Investment Bank, the Nordic Investment bank and the European Investment Bank) and insurance companies. The graph below shows how the equity mix has morphed in the last couple of years.

Change in Equity Mix for Wind Energy

The share of equity provided by utilities is steadily shrinking as other players get involved, decreasing from 62% in 2010 to 39% in 2015, and that of non-utility corporates from 31% to 15%. In other words, the combined share of the two traditional equity investors in the wind energy sector decreased substantially, from 93% in 2010 to 54% in 2015. Accordingly, other investors have stepped up their game. One of the possible explanations for this decrease may potentially be due to deleveraging as a consequence of the financial crisis.

The Rise of Institutional Investors

For brownfield wind projects, meaning wind projects where there is already existing infrastructure and possibly licenses as well, institutional investors such as pension funds, insurance companies, private equity and infrastructure funds have become major equity investors. According to the OECD, their cut in total equity provisions increased from 6% in 2010 to a staggering 37% in 2015, making them the second most important equity providers in the 2015 sample, just 1% behind utilities. This sharp increase of equity provision by institutional investors can be traced mainly to the acquisition of brownfield assets or portfolios for onshore wind deals. Pension funds and insurers were not involved in any greenfield onshore wind-power transactions included in the OECD 2015 sample.

This trend suggests that institutional investors look to the onshore wind sector mainly for the acquisition of existing projects.Such a strategy presents several advantages:

- Lower Costs: Existing projects are already (usually) built, and there they do not need to start from scratch;

- “Up to Code”: Lengthy permits, licensing and commissioning agreements may already be in place and therefore do not need to be requested;

- Fast Deployment: Ultimately the project can be up and running (and earning) in less time.

Moreover, equity financing in wind energy assets by state agencies and public finance institutions grew from a negligible cut in 2010 to 9% of total equity invested in 2015. This sharp increase can be linked directly to the investments done by the UK Green Investment Bank. The UK’s GIB, an institution created by the UK government in 2012 with the aim of attracting private sector financing for green infrastructure projects. The creation or expansion of similar institutions is a trend observable at the global level and is important for risk sharing with newer technologies. Take offshore wind, for example, as projects scale up and move into deeper water, newer technologies also add to construction risk. This may be a barrier to entry and discourage some investors from participating.

In Europe, commercial banks have started partnering up with government supported banks (United Kingdom’s Green Investment Bank, Germany’s KfW Development Bank), export credit agencies (Denmark’s EKF and Belgium’s Delcredere – Ducroire and Italy’s SACE), and multilateral banks (the European Investment Bank) as a way to provide equity financing to wind projects .

The diversification of participants is good for everyone, because:

- Risk: The risk that corresponds to the project is diversified across an array of investors, meaning that investors are more likely to invest if they do it along other reputable investors, rather than going in it solo;

- Mainstreaming: the diversification of participants shows that equity financing for RE is no longer as niche as it was, with pension funds and insurance companies putting skin in the game.

Example: The Galloper Offshore Wind Farm

The largest wind equity deal in Europe in 2015 the the Galloper Offshore Wind Farm. It’s a project that will be completed in 2018, located off the coast if Suffolk, east England.

The equity investors are:

- Innogy Renewables UK, a subsidiary of the German utility company RWE

- The UK’s Green Investment Bank, a public finance institution

- Macquarie Capital, an institutional investor

- Siemens Financial Services, a subsidiary of Siemens, a corporation

- Sumitomo Corporation, a corporation

This array of private and public investors is an example of what the equity landscape is shifting towards.

So why did the equity investing landscape change?

The explosion of new capacity additions fostered equity market growth for wind projects. New projects not only became more frequent but they also grew in average size, requiring more capital. It would only be normal to have several new, independent developers enter the sector under such favorable market conditions. Moreover, many utilities have been financially constrained due to the difficulties in the merchant power sector, further limiting their contribution to the sector.

The take-home message we can draw from this is that as the demand for wind energy increased so did the associated capital requirements. Utilities and developers did not have the necessary capital to cover demand, so third party investors were roped in. Likewise, corporations like Siemens and Sumitomo are using their financial strength to offer financing directly to smaller developers.